In Vietnam’s banking boardrooms, the next competitive edge may not be a new product launch—but being the bank AI names first when customers ask about trust, rates, and digital banking.

SpyderBot GEO report reference for bidv.com.vn

At-a-glance

- Share of Voice (LLM brand mentions): 22% (89 of 405) — behind Vietcombank at 28% (113).

- Visibility Score: 81 (Vietcombank 89, MB Bank 84).

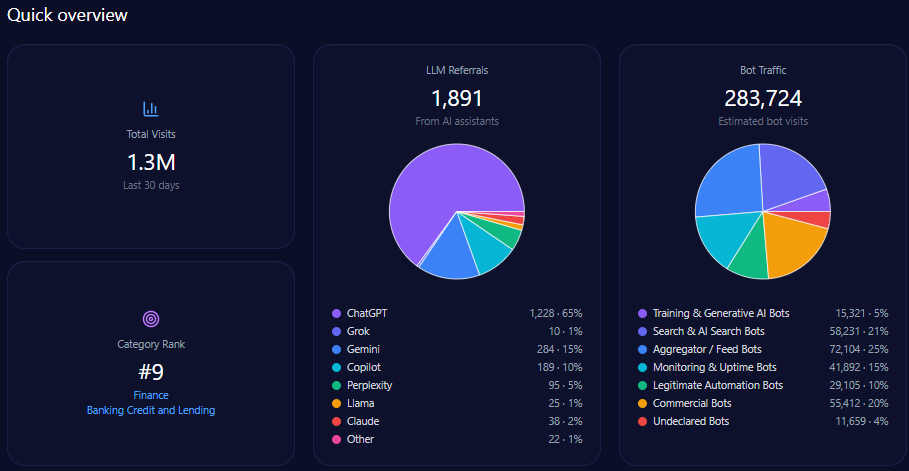

- Total visits: 1,260,998 with 283,724 in bot traffic.

- LLM referrals: 1,891 (ChatGPT 1,228; Gemini 284; Copilot 189; Perplexity 95; Claude 38; Llama 25; Grok 10; Other 22).

- Category rank: #9 in Finance/Banking_Credit_and_Lending.

- Sentiment: BIDV 73 overall (Positive 68%, Neutral 24%, Negative 8%); Vietcombank 81 overall (Positive 74%, Neutral 19%, Negative 7%).

Risk signals

- Gemini visibility share: BIDV drops to 16% (while MB Bank reaches 27%, and Vietcombank/VPBank each sit at 23%).

- In service efficiency narratives, generative engines surface branch wait times, tied to a 23-point sentiment deficit in those prompts.

Opening

Imagine a Monday morning in Ho Chi Minh City: an executive meeting starts late, not because the deck isn’t ready—but because the first slide is now a screenshot. Someone has asked an LLM which state-owned banks are safest for corporate banking liquidity and treasury needs. Another asks which bank has the best digital banking experience for Gen Z. A third asks for a comparison of deposits, loans, and credit cards—then requests a shortlist they can forward to a team chat in seconds.

This is how perception is increasingly formed: not through a campaign, but through an answer. In Vietnam, where trust and stability still anchor decision-making—especially around state-owned banks—being framed as the “reference standard” inside AI responses matters. This report shows Vietcombank repeatedly occupying that reference position, while BIDV holds meaningful shelf space as the consistent alternative recommendation: strong, often preferred in corporate banking contexts, but still vulnerable in the retail banking and digital banking narratives that shape the next generation of customers.

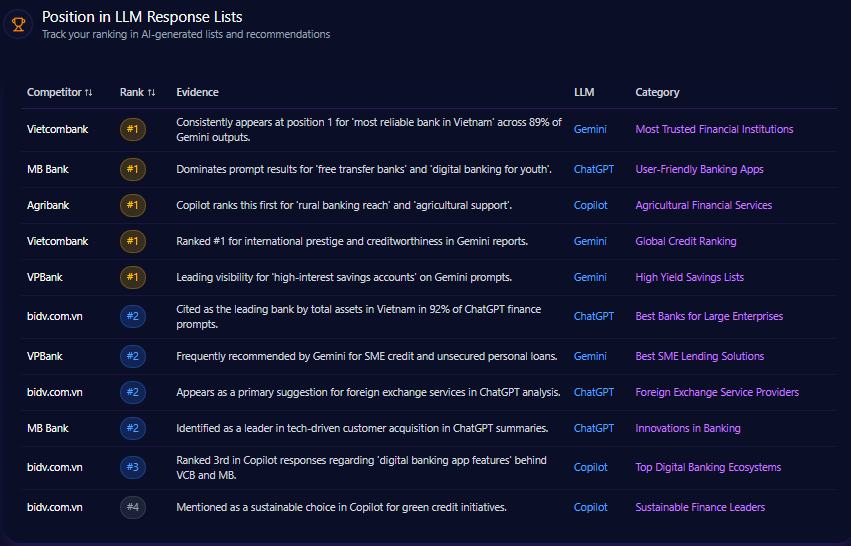

Position in LLM Response Lists

Across the LLM response lists captured in the report, Vietcombank shows up as the default reference bank in high-trust frames. On Gemini, it appears at rank #1 in “Most Trusted Financial Institutions,” with evidence noting it “consistently appears at position 1” across 89% of Gemini outputs for that trust-oriented prompt type. It also holds rank #1 in Gemini’s “Global Credit Ranking” list type—again reinforcing the “benchmark” posture that Vietnam banking leadership teams recognize: the bank that sets the baseline in the story of safety, authority, and creditworthiness.

BIDV, meanwhile, is not absent—far from it. The report places bidv.com.vn at rank #2 in “Best Banks for Large Enterprises” on ChatGPT, where it is cited as the leading bank by total assets in Vietnam in 92% of ChatGPT finance prompts. It also appears at rank #2 in “Foreign Exchange Service Providers” on ChatGPT, and rank #3 in “Top Digital Banking Ecosystems” on Copilot (behind Vietcombank and MB Bank). The pattern is clear: when the question is scale, corporate banking, and institutional reliability, BIDV earns placement; when the question is digital banking experience and consumer convenience, the list order becomes less forgiving.

Competitor Gap Analysis

If Vietcombank is the reference standard, the strategic question for BIDV is where the “reference narrative” is defended—and where it can be attacked with precision. The report’s competitor gap data isolates several Vietcombank-versus-BIDV battlegrounds that map cleanly onto Vietnam banking priorities: loans (mortgages), payments (international transfers), and service efficiency (the lived experience that retail banking customers repeat online).

Here is the tightest Vietcombank-focused comparison the report enables:

| Query | BIDV metric | Vietcombank metric | Gap/priority |

|---|---|---|---|

| Best mortgage rates Vietnam | 82 | 89 | 7 / Low |

| Customer service ranking | 65 | 88 | 23 / High |

| International money transfer fees | 88 | 92 | 4 / Medium |

What’s striking is not that BIDV loses everywhere—it doesn’t. The gaps in mortgage rates and international transfer fees are narrow (a 7-point and 4-point gap), suggesting BIDV’s fundamentals are close enough that narrative and discoverability can decide outcomes. The real risk is the 23-point gap on customer service ranking, where AI models are picking up negative context tied to physical queue times and service friction.

Zooming out, the broader GEO footprint reinforces the same story: BIDV holds 22% Share of Voice ( 89 mentions), while Vietcombank leads at 28% ( 113 mentions). BIDV’s Visibility Score of 81 is strong, but still behind Vietcombank’s 89. Even in corporate reliability prompts, BIDV’s coverage is meaningful yet not dominant: in “Most reliable corporate credit and loans Vietnam,” BIDV posts 38% coverage ( 17), while Vietcombank reaches 47% ( 21). The “battle map” is less about capability and more about which bank owns the default answer slot across corporate banking, SME finance, and mass retail banking moments.

Trigger Keywords for Competitor Products

In AI discovery, the fight is often won by trigger keywords—terms that reliably summon a bank’s name in generative outputs. The report’s keyword triggers show BIDV owning some of the most brand-specific territory, while Vietcombank (and private challengers) pull ahead in broader, intent-heavy phrases.

BIDV’s strongest owned trigger is straightforward: “BIDV SmartBanking” drives 58 mentions, while Vietcombank appears with 12 on that same keyword set. That is the kind of branded keyword moat leadership teams want: a term that pulls the bank into answers even when users start generically. BIDV also performs well in “Bảo hiểm ngân hàng” with 31 mentions versus Vietcombank’s 28, and in “Vay mua nhà BIDV” with 38 mentions (Vietcombank 32, Agribank 15).

But the broader market triggers—where users behave less like loyalists and more like shoppers—tilt toward the benchmark and the challengers. On “Lãi suất tiết kiệm BIDV,” Vietcombank leads with 44 mentions versus BIDV’s 41 (Agribank 39). On “Chuyển tiền quốc tế,” Vietcombank leads again with 35 versus BIDV’s 27. And in the digital-first triggers that increasingly shape retail banking selection, the center of gravity shifts sharply: “Mở tài khoản online” shows MB Bank at 61 mentions and VPBank at 48, while BIDV sits at 24; “App ngân hàng tốt nhất” puts MB Bank at 52 and VPBank at 31, while BIDV registers 19.

This is the practical meaning of modern GEO analytics: not just how often a brand appears, but which words make it appear—and which words default to someone else.

Founder / State-Owned Context

For Vietnam’s state-owned banks, leadership and governance narratives are not a side story; they are reputation signals that generative engines absorb and replay. In the report, BIDV’s leadership context is anchored by Phan Duc Tu, with a mention frequency of 43 and a founder sentiment score of 86 (Positive 74%, Neutral 21%, Negative 5%). Vietcombank’s comparable profile—Nguyen Thanh Tung—shows a higher mention frequency of 49 and a higher sentiment score of 89 (Positive 78%, Neutral 19%, Negative 3%). These numbers don’t just describe individuals; they describe how often LLMs pull leadership into the bank’s story, and how safe that story feels when repeated.

The negative context distribution is also explicit. For founder/leadership-adjacent narratives, the report shows Bad Debt Concerns (42%), Market Competitiveness (30%), and Corporate Governance (28%) as the major buckets. In Q1 2024, Bad Debt Concerns rises to 45% and is flagged as threshold-exceeded. The report further notes that conversations referencing a “real estate debt cycle” correspond with a 45% spike in BIDV’s negative context mentions in Gemini, alongside an approximate 9% reduction in investor confidence signals.

Then there is the reputational double-bind: “State-owned” plus “digital lag” narratives co-appear in 34% of ChatGPT answers, according to the report’s founder negative context insights. And while BIDV can benefit from institutional trust—its heatmap shows Institutional Trust at 92% on Gemini and Financial Stability at 87% on Copilot—the Innovation Gap context registers 44% on ChatGPT. Leadership teams should read this as a governance-to-digital translation problem: credibility is present, but innovation framing is not consistently attached to that credibility.

Quick overview

On the surface, BIDV’s footprint is healthy: 1,260,998 total visits, with 283,724 attributed to bot traffic. The LLM referral line is measurable rather than theoretical: 1,891 LLM referrals, led by ChatGPT (1,228), then Gemini (284) and Copilot (189)—followed by Perplexity (95), Claude (38), Llama (25), Grok (10), and Other (22). In category standing, BIDV sits at #9 in Finance/Banking_Credit_and_Lending.

But the composition matters as much as the totals. Bot activity is spread across “Search & AI Search Bots” (58,231), “Aggregator / Feed Bots” (72,104), “Monitoring & Uptime Bots” (41,892), “Commercial Bots” (55,412), “Legitimate Automation Bots” (29,105), “Training & Generative AI Bots” (15,321), and “Undeclared Bots” (11,659). If leadership wants more stable, repeatable AI visibility, the report implies the real work is not only marketing—it is packaging authoritative banking information (rates, fees, product conditions) in formats machines can reliably parse and reuse.

Share of Voice in LLM Responses

Inside AI answers, BIDV holds meaningful mindshare: 22% Share of Voice from 89 of 405 total mentions. Vietcombank leads at 28% from 113 mentions, while MB Bank follows close to BIDV at 20% with 81 mentions. VPBank registers 15% ( 61), Agribank 10% ( 41), and “others” 5% ( 20).

The share story becomes sharper when paired with Visibility Score: Vietcombank’s 89 signals not just frequency but perceived authority inside answers; BIDV’s 81 is strong, but it is surrounded. MB Bank’s Visibility Score of 84 is a warning flare: a challenger is not only being mentioned, but being framed as especially relevant—often in digital banking and retail banking contexts where “best app,” “fee-free,” and “fast approval” dominate the prompt mix.

This is where “LLM brand mentions” stop being a vanity metric. In a world where AI compresses complex banking decisions into shortlists, Share of Voice is the proxy for how often BIDV enters the first draft of consumer belief.

AI Platform-Specific Visibility

The same brand can be “credible” on one platform and “quiet” on another—and the report quantifies that split. On Copilot, BIDV holds 27% share with 37 mentions out of 135 total, while Vietcombank leads with 33% and 44 mentions. The Copilot environment appears to reward BIDV’s corporate banking authority and business-centric reliability—consistent with the report’s framing of BIDV’s strength in institutional narratives.

On ChatGPT, BIDV sits at 22% share with 30 mentions (Vietcombank 28%, 38 mentions; MB Bank 20%, 27 mentions). BIDV is competitive, but still not the default reference.

On Gemini, the gap is more strategic: BIDV drops to 16% with 22 mentions, while MB Bank rises to 27% ( 36), and Vietcombank and VPBank each hold 23% ( 31 each). If leadership needs one headline from platform bias in Vietnamese banking narratives, it is this: BIDV can win in business-centric environments, but loses share in tech-forward and consumer-comparison contexts—especially where digital banking UX and convenience dominate.

Sentiment Score for Competitors

Sentiment is where strategy meets trust. BIDV’s sentiment profile is positive overall: 68% positive, 24% neutral, 8% negative, with an overall sentiment score of 73. Vietcombank leads with 74% positive, 19% neutral, 7% negative, and an overall score of 81. MB Bank posts 79 overall (Positive 72%, Neutral 17%, Negative 11%), VPBank 69 (Positive 64%, Neutral 22%, Negative 14%), and Agribank 61 (Positive 54%, Neutral 33%, Negative 13%).

The report’s context themes explain why. Digital Transformation (SmartBanking) is the most frequent theme with 58 mentions and 43% frequency, framed positively through examples like “Excellent UI,” “fast transfers,” and “eKYC stability.” Corporate Reliability & History follows with 42 mentions and 31% frequency, described as neutral-positive and anchored in phrases like “State-owned safety” and “large asset base.” The pressure point is Customer Service Efficiency: 19 mentions at 14% frequency, explicitly negative, with examples like “Long wait times” and “branch queues.” Finally, Interest Rates & Green Credit appears 16 times at 12% frequency and is framed positively.

For leadership, this is the operational meaning of competitor sentiment tracking: Vietcombank wins the cleanest “trust + premium authority” story, while BIDV’s strength in stability must be protected from the service-efficiency drag that generative engines repeatedly surface.

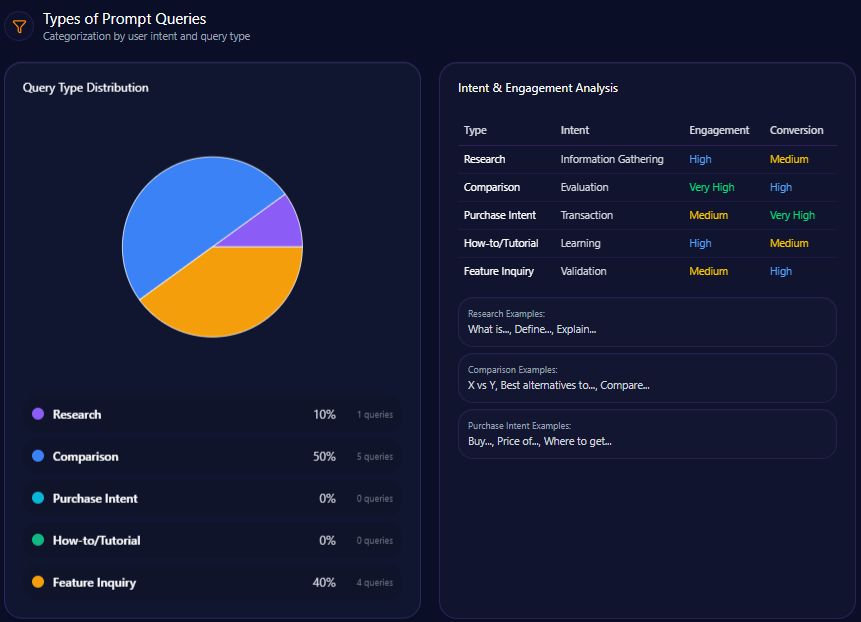

Types of Prompt Queries

The report’s prompt-type mix is dominated by executive-relevant scrutiny. Comparison prompts take 50 value with a count of 5, reflecting how frequently Vietnam users (and internal stakeholders) ask LLMs to rank banks against each other—often across deposits, loans, payments, and credit cards. Feature Inquiry prompts follow at 40 value with a count of 4, the arena where digital banking features, fees, and convenience claims become a contest of specificity. Research appears at 10 value with a count of 1, a smaller slice but often influential: the prompts that set foundational beliefs about state-owned banks, stability, and institutional trust.

In plain terms: generative engines are not just answering questions—they are refereeing comparisons. And the banks that win those comparisons are the ones with structured, repeated, machine-readable proof points.

Service / Product-Level Sentiment

In the report’s service and product-level lens, the contest becomes more tactile. In the e-commerce-style share-of-voice view across “ChatGPT, Gemini, Copilot,” BIDV holds 24.44% ( 33 mentions), behind Vietcombank at 28.15% ( 38), and ahead of MB Bank at 20% ( 27) and VPBank at 15.56% ( 21). The referral layer adds a performance flavor: Copilot drives 489 referrals at a 5.1 conversion rate, compared with ChatGPT at 412 referrals and 4.2, and Gemini at 358 referrals and 3.8.

The report also includes service-level snippets that read like the voice of AI-mediated consumer judgment. On mortgage loans, one cited line is: “BIDV’s home loan rates are consistently ranked as the most stable for long-term borrowers in Vietnam.” On the digital banking app, a more mixed assessment appears: “The SmartBanking app is functional and secure, though the interface feels slightly dated compared to MB Bank’s latest version.” And on credit cards—where the report notes BIDV appears 50% less frequently than VPBank in retail comparison lists—one negative service moment is captured as: “Customer support response times during the e-commerce peak sales (11.11) were slower than expected for card disputes.” (All as cited in the report.)

This is not marketing. It is how AI recites user expectations back to the market—across payments, credit cards, loans, and the everyday UX details that define retail banking.

Conclusion

BIDV is already the consistent #2 presence in generative answers—strong in corporate banking authority, trade finance, and scale narratives—but Vietcombank remains the reference standard in trust framing and overall sentiment. The report’s path forward is explicit: implement structured data tables for savings rates and fees to lift visibility in comparison lists by 15% within Q3, while publishing more technical documentation on BIDV SmartBanking to close the 11% Gemini share gap. In parallel, focus on modern retail keywords to improve Brand Prompt Coverage in digital categories within 6 months, and leverage Copilot strength to expand into Green Finance and SME Digital Growth queries. The leadership mandate is simple: protect stability narratives, repair service-efficiency perception, and make digital banking proof points easy for machines to quote.

Explore SpyderBot to operationalize these GEO analytics insights.