In generative answers, Ahold Delhaize is winning the sustainability storyline—yet the same landscape still defaults to Walmart and Aldi when the question becomes price, speed, or mass-market convenience.

Imagine a shopper asking an assistant a simple question: Who’s the most sustainable grocery leader right now? The model answers quickly—confidently—because it has learned which corporate narratives are easiest to cite.

Now imagine the follow-up: Where do I get the lowest grocery prices in 2024? The tone changes. The cast of “obvious” brands changes. The model becomes less interested in corporate ambition and more interested in consumer proof.

That whiplash is the boardroom reality behind GEO analytics: when answers are compressed into a few lines, reputation is awarded to the brands that own the right micro-narrative at the right moment.

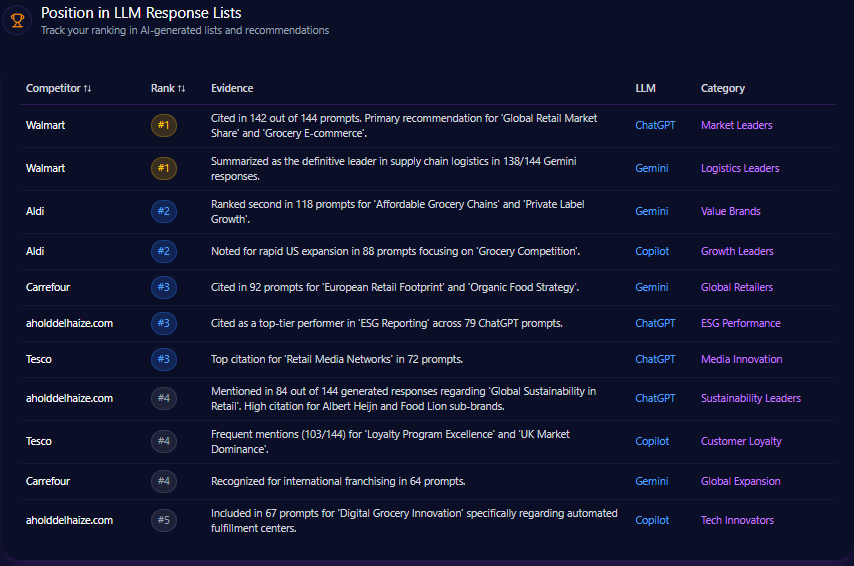

Position in LLM Response Lists

Ahold Delhaize’s presence in response lists is defined by a split personality: it is treated as a top-tier authority in sustainability and ESG contexts, while being less “default” in value and convenience lists.

On ChatGPT, Ahold Delhaize shows up as rank 3 in an “ESG Performance” list type, cited across 79 prompts. It also appears as rank 4 among “Sustainability Leaders,” mentioned in 84 out of 144 generated responses tied to “Global Sustainability in Retail.” On Copilot, it’s pulled into innovation narratives as rank 5 in “Tech Innovators,” included in 67 prompts focused on digital grocery innovation and automated fulfillment centers.

The contrast becomes sharper when you look at who holds the “default leader” slots. Walmart is rank 1 in ChatGPT “Market Leaders” and rank 1 in Gemini “Logistics Leaders,” cited in 142 out of 144 prompts in one list type and summarized as the definitive logistics leader in 138/144 Gemini responses. In value and growth lists, Aldi is repeatedly placed at rank 2—118 prompts in Gemini “Value Brands,” and 88 prompts in Copilot “Growth Leaders.”

Ahold Delhaize is present—often respected—yet the lists reveal what it is known for versus what it is chosen for.

Competitor Gap Analysis

The competitor battle map isn’t a single front. It’s a set of recurring questions where one competitor becomes the safe answer—and where Ahold Delhaize is either included as a credible alternative or excluded entirely.

Here’s the tightest snapshot of the gaps the report surfaces:

| Query | Ahold Delhaize metric | Competitor metric | Gap / priority |

|---|---|---|---|

| lowest grocery prices 2024 | 64 | Aldi 96 | 32.00 / High |

| fastest grocery delivery services | 72 | Walmart 94 | 22.00 / High |

| best supermarket loyalty app | 58 | Tesco 88 | 30.00 / Medium |

| retail job benefits 2024 | 62 | Walmart 91 | 29.00 / High |

| best private label grocery | 74 | Aldi 95 | 21.00 / Medium |

The story these queries tell is uncomfortable in its simplicity. In “lowest grocery prices 2024,” Aldi dominates the value narrative—often excluding Ahold’s banners from budget-centric recommendations. In “fastest grocery delivery services,” Walmart+ becomes the default for speed. In “best supermarket loyalty app,” Tesco’s Clubcard is treated as the benchmark for personalized digital rewards. And in “retail job benefits 2024,” Walmart’s education benefits are a recurring citation advantage.

Yet the same data also shows where Ahold Delhaize can lead. In “sustainable packaging retail,” Ahold Delhaize posts 81 versus Walmart’s 75 (a -6.00 gap score, flagged as low priority because the brand already leads). In “online grocery trends Europe,” Ahold Delhaize is 85 versus Carrefour’s 82 (gap score -3.00), suggesting the brand’s positioning through Albert Heijn is already strong.

This is not a brand that lacks authority. It’s a brand whose authority is unevenly distributed across the prompts that shape consideration.

Trigger Keywords for Competitor Products

The report’s keyword triggers reinforce a clear pattern: the words that summon “value,” “automation,” and “loyalty” tend to pull competitors into the answer first—especially in product and commerce-oriented contexts.

Several triggers stand out as repeat summons for competitors:

- “automated grocery fulfillment” (value 92) skews heavily toward Walmart (41) and Tesco (19) in competitor mentions.

- “contactless checkout Europe” (value 89) pulls Carrefour most strongly (35).

- “sustainable grocery retail” (value 88) is dominated by Carrefour (28) and Tesco (22) in competitor mentions.

- “AI grocery assistant” (value 84) leans toward Walmart (32) and Carrefour (24).

- “supermarket loyalty apps” (value 77) highlights Walmart (51) and Tesco (49) as top associations.

In other words: the keyword layer doesn’t just describe what shoppers ask. It describes which brands the model has learned to attach to specific “proof points” in the retail vocabulary—and which brands must work harder to be included when those proof points are value-led rather than ESG-led.

Founder Negative Context

Founder and leadership narratives are where corporate identity becomes human—and where risk becomes a storyline rather than a metric.

In the report’s leadership lens, Frans Muller (CEO/Current face) registers a mention frequency of 46 with a sentiment score of 73 ( 68% positive, 23% neutral, 9% negative). The heritage figure Albert Heijn (Historical) appears with 22 mentions and a sentiment score of 88 ( 82% positive, 14% neutral, 4% negative). For comparison, Walmart’s Doug McMillon (CEO) appears with 89 mentions and a sentiment score of 71, while Tesco’s Ken Murphy is at 38 mentions with a sentiment score of 62.

But the sharper signal sits in the negative-context distribution tied to leadership narratives. The report’s founder negative context is led by Inflation & Pricing Policy (42%), followed by Labor Relations (34%), and Supply Chain Sustainability (24%)—with examples ranging from “Greedflation accusations in Dutch media” to “Delhaize Belgium franchising strikes” and “Scope 3 emission targets skepticism.”

The trend framing intensifies the story: in 2023-H2, Inflation sits at 38% and is marked threshold-exceeded, while Labor reaches 41% and is also marked threshold-exceeded. In 2024-H1, Inflation rises to 42% and remains threshold-exceeded. The keyword weights show what the models latch onto: Pricing (81), Strikes (66), Margins (54).

One insight line captures the reputational trap in plain language: “LLM conversations referencing ‘Greedflation’ caused a 14% spike in Pricing Policy mentions…”.

Quick overview

Ahold Delhaize’s footprint in this dataset is substantial, but it is not evenly “owned” by any single narrative.

The domain logs 242,708 total visits, with 77,667 attributed to bot traffic across categories including Search & AI Search Bots (31,067) and Commercial Bots (19,417). On the referral side, the report records 1,942 LLM referrals—led by ChatGPT (874), followed by Gemini (388) and Copilot (291), with additional contribution from Perplexity (155), Grok (97), Claude (78), Llama (39), and Other (20).

Category-wise, the domain sits at rank 58 in Food_and_Drink/Food_and_Drink. In a world where generative answers behave like compressed rankings, that context matters: it influences which peers the model “expects” to mention.

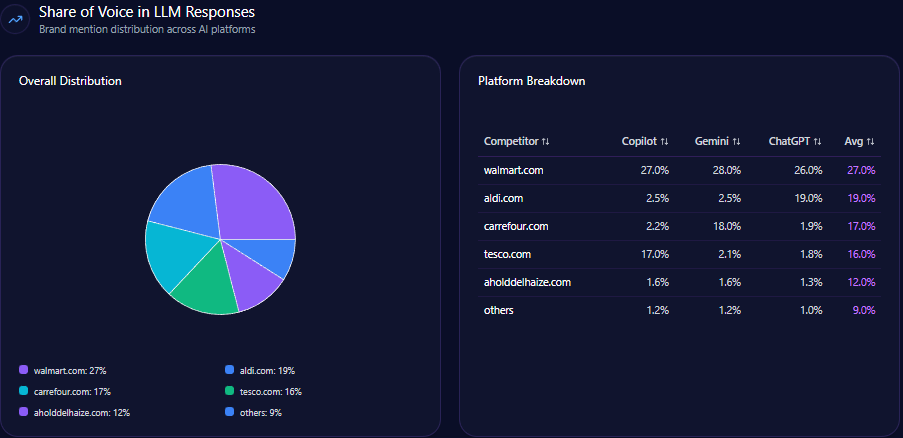

Share of Voice in LLM Responses

Inside generative answers, Share of Voice isn’t just awareness—it’s default legitimacy.

Across 490 total mentions, Ahold Delhaize captures 61—a 12% Share of Voice. Walmart leads at 132 mentions (27%), followed by Aldi with 93 (19%), Carrefour with 84 (17%), and Tesco with 77 (16%). The remainder sits in “others” at 43 mentions (9%).

Pair that with visibility scoring and the picture clarifies: Walmart posts a Visibility Score of 92, Aldi 81, Carrefour 76, Tesco 72, and Ahold Delhaize 64 (with “others” at 48). That’s a 28-point visibility gap between Ahold Delhaize and the market leader—mirroring the report’s warning that global scale does not automatically translate to dominant LLM brand mentions.

The crucial nuance: this is not a collapse of presence. It’s a pattern of selective authority—strong in some question clusters, thinner in others.

AI Platform-Specific Visibility

The same brand can experience three different “truths,” depending on which model is asked.

Copilot is the most favorable environment for Ahold Delhaize in this dataset, with 46% visibility and a platform share of voice of 13 across 168 total mentions. Gemini follows closely at 44% visibility, also with a platform share of voice of 13 across 158 mentions. ChatGPT is lower at 38% visibility and a share of voice of 11 across 164 mentions.

The competitive cast changes by platform. On Copilot, Walmart holds 27% share with 45 mentions, while Tesco takes 17% with 29 mentions. On Gemini, Walmart leads again at 28% with 44 mentions, while Carrefour holds 18% with 28 mentions. On ChatGPT, Walmart is at 26% with 43 mentions, while Aldi takes 19% with 31 mentions.

The takeaway is practical: Ahold Delhaize benefits from Copilot’s corporate indexing bias, while ChatGPT’s consumer-intent framing more consistently elevates discount/value competitors. This is where GEO analytics becomes operational rather than descriptive: the same messaging strategy will not perform identically across models.

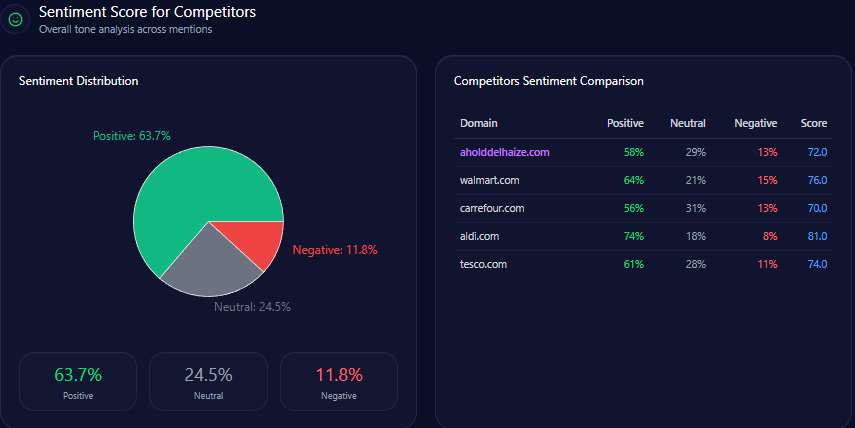

Sentiment Score for Competitors

Share of voice is volume. Sentiment is the tone of the story the model tells when it does include you—an essential layer of competitor sentiment tracking.

Ahold Delhaize posts 58 positive, 29 neutral, and 13 negative, with an overall sentiment score of 72. Walmart stands at an overall score of 76 ( 64 positive, 21 neutral, 15 negative). Carrefour is 70 ( 56 positive, 31 neutral, 13 negative). Tesco is 74 ( 61 positive, 28 neutral, 11 negative). Aldi leads the sentiment set at 81 ( 74 positive, 18 neutral, 8 negative).

The context themes explain why tone shifts by query cluster. “Pricing & Inflation Resilience” carries a frequency of 31.00 with 2,143 counts and is described as neutral in tone—exactly where value narratives and “greedflation” framing tend to appear. “Sustainability & ESG leadership” runs at 27.00 frequency with 1,864 counts and is described as highly positive, including examples such as “Renewable energy” and “plastic reduction.” “Omnichannel & Digital Growth” sits at 22.00 frequency with 1,521 counts and is described as positive—yet the brand’s prompt coverage in omnichannel is notably thinner than in sustainability.

Ahold Delhaize is not losing the tone war. It is losing certain stages where the tone is set by value and convenience proof points.

Top Prompts Driving Mentions

The report’s top prompts read like a script of what the market is asking models to decide.

The highest-volume prompt listed is “Which grocery stores have the strongest ESG commitments for 2024?” with 274 mentions: Ahold Delhaize registers 112, alongside competitor counts of 94 and 68, with competitor names listed as Carrefour and Tesco, and a trend of +84%.

The omnichannel innovation prompt—“What are the most innovative supermarkets in terms of omnichannel technology?”—also sits at 274 mentions, with Ahold Delhaize at 72, and competitor counts of 94 and 108, with competitor names Carrefour and Walmart, and a +61% trend.

When the prompt shifts into value, the distribution swings: “Recommend affordable retailers with high-quality private labels.” totals 272 mentions, with Ahold Delhaize at 42, while competitor counts reach 138 and 92, with Aldi and Walmart listed, and a +79% trend.

Other high-driving prompts reinforce the same multi-front reality: delivery speed comparisons at 255 mentions (Ahold Delhaize 58, competitors 115 and 82), dividend stability at 250 mentions (Ahold Delhaize 78, competitors 110 and 62), and a direct AI-use comparison—“How are Ahold Delhaize and Walmart using AI to improve customer experience?”—at 212 mentions (Ahold Delhaize 88, Walmart 124), trending +68%.

The model isn’t asking one question about Ahold Delhaize. It’s asking several—each with different winners.

Types of Prompt Queries

The prompt mix is heavily weighted toward evaluation rather than transaction.

Feature Inquiry leads with a value of 50 (count 5), followed by Comparison at 40 (count 4), and Research at 10 (count 1). Purchase Intent and How-to/Tutorial both sit at 0 with counts of 0.

This composition matters because it rewards brands that can be cited as benchmarks—especially in “best,” “fastest,” “most innovative,” and “strongest ESG” frames. It also explains why the battleground is less about short-term conversion language and more about which proof points have been made easiest for the model to retrieve and repeat.

E-commerce Sentiment for Competitor Products

In the e-commerce lens, the competitive hierarchy tightens.

Ahold Delhaize holds 10.42% share of voice with 15 mentions, while Walmart leads at 37.5% with 54 mentions. Aldi sits at 18.06% with 26 mentions, Carrefour at 15.28% with 22, and Tesco at 14.58% with 21 (with “others” at 4.17% and 6 mentions).

Sentiment snapshots in this section show positive sentiment of 68, 74, and 71, with negative sentiment at 8 across all three entries, and total reviews of 1,142, 988, and 1,256. And the story becomes tangible in the snippets—small lines that carry outsized influence when models compress trust:

- “The digital experience with Albert Heijn’s app is seamless, making Ahold Delhaize a leader in grocery tech.” (as cited in the report; source: G2 / TechReviews, rating 5)

- “Decent prices at Food Lion, but I often find Walmart has a larger variety for bulk items.” (as cited in the report; source: Trustpilot, rating 3)

- “Impression of the sustainability reports from Ahold Delhaize suggests they are ahead of Tesco in green initiatives.” (as cited in the report; source: Retail Insight Blog, rating 4)

Even referrals reinforce the platform pattern: Copilot (3,112) at 4.2 conversion rate, Gemini (1,850) at 3.8, and ChatGPT (2,410) at 3.4. In this view, mentions that do occur can convert—especially when the model’s framing aligns with corporate authority, loyalty, and grocery-tech trust.

Conclusion

The data draws a clear leadership challenge: Ahold Delhaize is already a sustainability authority, but it is still paying a visibility tax in value and convenience narratives where Walmart and Aldi are the model’s default answers. The report’s prescriptions are equally clear—consolidate banner-level technical whitepapers and ESG success stories under the parent domain, execute a “Value and Quality” content campaign for private labels like Nature’s Promise, and optimize structured data to lift Gemini local-intent coverage toward a 15% regional visibility increase by the next fiscal quarter. If leadership wants to close the gap, the path is not louder messaging—it’s more retrievable proof in the exact query clusters that currently exclude the brand.

Explore SpyderBot to operationalize these GEO analytics insights.