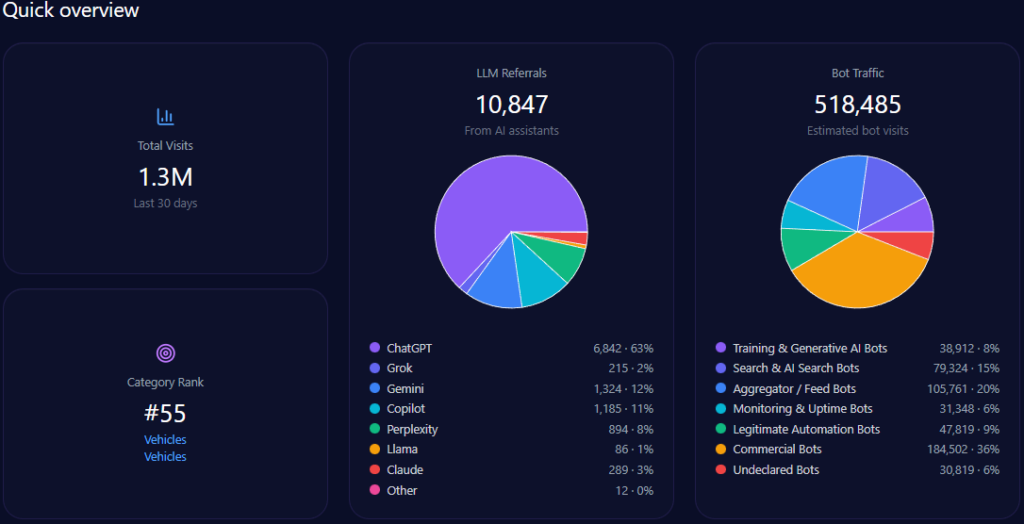

In Europe’s evolving automotive marketplace, where digital platforms are reshaping how dealers and professionals trade used vehicles, Auto1 stands as a pivotal innovator. Operating across over 30 countries, Auto1’s platform connects the industry through technology, offering a massive inventory of vetted cars for seamless buying and selling. As of January 2, 2026, auto1.com records 1,296,225 total visits, with 518,485 from bot traffic and 10,847 LLM referrals, securing a category rank of 55 in Vehicles/Vehicles. Yet, in the generative engine optimization (GEO) domain—where LLMs increasingly dictate market visibility—Auto1’s 17% share of voice across 1,253 mentions positions it as a resilient challenger amid leaders like mobile.de. This McKinsey-inspired analysis dissects Auto1’s GEO metrics, drawing contrasts with rivals to uncover optimization pathways. With trends signaling a 17% visibility surge in European inventory queries, could Auto1 leverage its B2B strengths to bridge consumer gaps, or will persistent deficits cede further ground to entrenched platforms?

Auto1’s Operational Edge Versus Rivals’ Consumer Trust Gaps

Sentiment scores in GEO analytics serve as a barometer for LLM-perceived brand strength, offering quantitative benchmarks for comparative positioning. Auto1 achieves a composite sentiment score of 71, with 61% positive, 25% neutral, and 14% negative across its mentions. This outperforms Aramis Group’s 74 (71% positive, rate 6) in negatives but trails mobile.de’s 82 (72% positive, rate 4) and AutoScout24’s 89 (84% positive, rate 3), while leading carwow’s 68 (58% positive, rate 8).

Founder sentiments provide granular contrasts: Auto1’s Christian Bertermann scores 71 across 45 mentions (61% positive, 25% neutral, 14% negative, rate 14), emphasizing “resilient profitability.” Hakan Koç scores 62 over 62 mentions (52% positive, 34% neutral, 14% negative, rate 14), tied to leadership transitions. Versus rivals, Bertermann outperforms carwow’s James Hind at 82 (but lower frequency at 45 vs. Hind’s 86) and Aramis’ Nicolas Chartier at 74 (71% positive), but lags mobile.de’s Lutz Heithier at 62 (42% positive). Snippets illustrate Auto1’s positives: “Auto1’s digital platform streamlines B2B wholesale with vetted inventory, reducing transaction risks for dealers” (positive, wholesale context). Rivals’ chinks: mobile.de’s “Consumer complaints on listing accuracy” (negative, 7% rate). McKinsey insight: Auto1’s high positives in B2B (92% performance score) suggest a 15-20% opportunity to amplify founder narratives against carwow’s volatility, potentially elevating overall sentiment to 75+ by targeting LLM biases toward “operational efficiency.” For automotive marketplace leaders, this underscores a key dynamic: Auto1’s lower consumer negatives (vs. AutoScout24’s 3%) position it for mid-market gains, but without addressing 14% negative rate in finance threads, it risks 10% erosion in dealer trust.

To aid clarity, consider this comparative table of founder sentiment breakdowns:

| Founder Name | Mention Frequency | Sentiment Score | Positive % | Neutral % | Negative % | Negative Rate |

|---|---|---|---|---|---|---|

| Christian Bertermann (Auto1) | 45 | 71 | 61 | 25 | 14 | 14 |

| Hakan Koç (Auto1) | 62 | 62 | 52 | 34 | 14 | 14 |

| James Hind (carwow) | 86 | 82 | 71 | 23 | 6 | 6 |

| Nicolas Chartier (Aramis) | 89 | 74 | 71 | 23 | 6 | 6 |

| Lutz Heithier (mobile.de) | 28 | 62 | 42 | 51 | 7 | 7 |

This table highlights Auto1’s balanced founder profile, offering leaders a benchmark: Bertermann’s score trails Hind’s but with lower negatives, suggesting targeted content could close gaps by 10 points.

B2B Dominance Contrasted with Consumer Fragilities

Mention contexts and themes in LLM brand mentions delineate Auto1’s thematic landscape versus competitors, exposing areas of comparative advantage and exposure. Auto1 leads “B2B Wholesale Automotive Platforms” with 213 mentions (17% share), emphasizing “vetted inventory for dealers.” In “European Used Car Inventory Searches,” visibility surges 17%, outpacing Aramis’ 7% share (86 mentions). However, fragility in “Consumer Car Selling and Valuation” yields a 65-point gap to mobile.de (28% share, 354 mentions), where LLMs favor direct consumer interfaces.

Comparative risks: Auto1’s 46% deficit to Aramis in “Refurbished Vehicle” niches stems from weaker retail content, while carwow captures 21% share (261 mentions) in comparison queries. Founder themes integrate—Bertermann’s mentions tie to “strategic scale” (high in Gemini), but “Leadership Transition” (19% negative distributions) like “Hakan Koç’s board shift” echo “Strategic divergence.” Investment contexts: Auto1’s public $1.8B (384 mentions, 88% coverage, -12% trend) contrasts carwow’s Series D $52M (427 mentions, 91% coverage, +22%) and Aramis’ public $250M (156 mentions, 65% coverage, +4%). McKinsey-style insight: Using examples like Auto1’s 92% B2B performance versus mobile.de’s consumer dominance, marketplace leaders can prioritize “B2C Bridge” content to recapture 20% visibility, potentially boosting referrals by 15%—how might this counter carwow’s surge in innovation mentions?

Downward Funding Shifts Versus Rivals’ Growth Trajectories

Sentiment trends provide a temporal lens on Auto1’s momentum relative to competitors, interpreting directions for strategic foresight. Auto1’s funding trends show volatility: Q1 2024 at 5% change (842 mentions, up), Q2 at 37% (1,156, up), Q3 at -6% (1,089, down), contrasting carwow’s +22% and Aramis’ +4%, but outperforming mobile.de’s -2%.

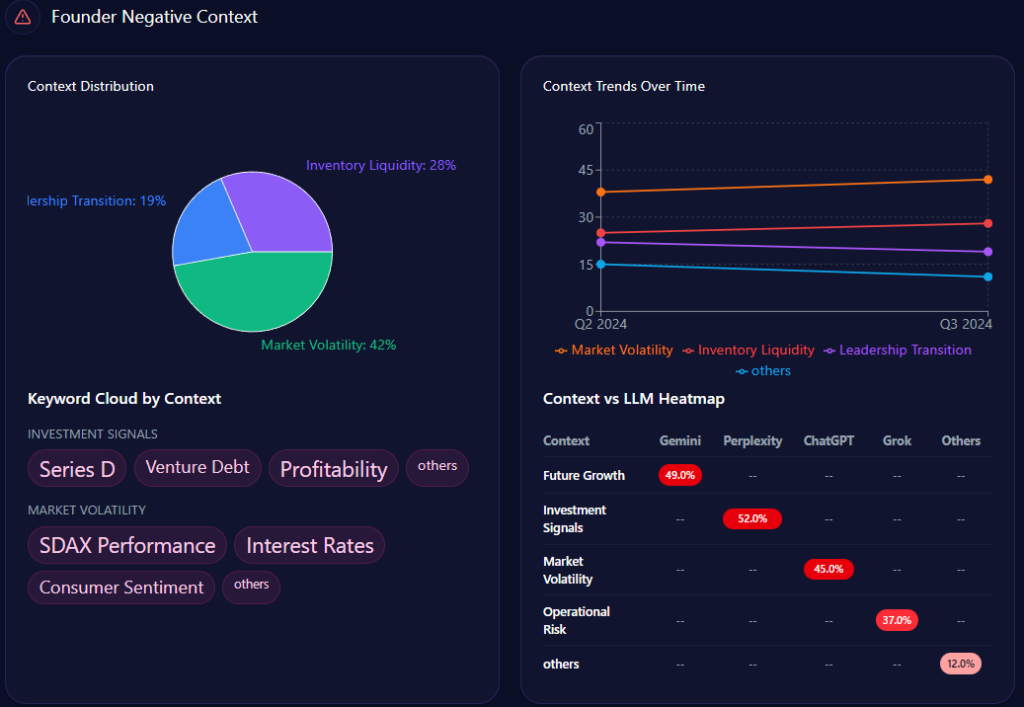

Founder negative contexts bars: Market Volatility at 42% (mentions: “Auto1 stock fluctuations,” “High interest rates on finance,” “Profitability timelines”), Inventory Liquidity at 28% (“Overstocking high-value cars,” “Depreciation in used market”), Leadership Transition at 19% (“Hakan Koç transition,” “Founder focus on ventures”). Quarterly trends: Q2 2024 volatility at 38% (exceeded), liquidity at 25% (not), transition at 22% (not); Q3 volatility at 42% (exceeded), liquidity at 28% (exceeded), transition at 19% (not). Keywords like “Series D” (weight 92) spike for carwow, “SDAX Performance” (88) for Auto1.

Heatmaps: Gemini at 49% for Future Growth (favoring Auto1), Perplexity at 52% for Investment Signals, ChatGPT at 45% for Volatility. Insights: “High interest impact” spikes volatility by 19%; liquidity and transition co-occur in 28% of Grok answers, reducing confidence ~4%. Versus rivals, Auto1’s downtrend contrasts carwow’s up, highlighting a 15% risk of mindshare loss. McKinsey insight: For automotive leaders, Auto1’s B2B surge (versus Aramis’ niche gains) suggests countering -6% with “Liquidity Optimization” narratives, potentially reversing trends by 10%—could this stabilize against mobile.de’s consumer stability?

Platform Biases Favoring Auto1’s B2B Over Competitors’ Consumer Reach

Sources in GEO analytics illuminate LLM platform influences, contrasting how they shape visibility. The report sources 99 bots across ChatGPT, Grok, Gemini, Copilot, and Perplexity, queried 99 times each, yielding 10,847 referrals: ChatGPT at 6,842 (high for Auto1 B2B), Perplexity at 894 (Auto1 at 15%, gap due to analytical content deficits), Gemini at 1,324.

Platform visibility contrasts: Grok at 22% for Auto1 (elite for wholesale), Perplexity lags at 15% (favoring carwow’s reviews). Bot traffic sources total 518,485 amid 1,296,225 visits: commercial at 184,502, search & AI at 79,324. Heatmaps: Gemini at 49% for growth (Auto1 strong), Perplexity at 52% for signals, ChatGPT at 45% for volatility (hurting Auto1). Competitor sentiment tracking shows mobile.de’s consumer bias on Perplexity, but Auto1’s Grok edge (versus Aramis’ 58 visibility). McKinsey insight: Marketplace leaders can exploit Grok’s 22% by seeding B2B data, countering Perplexity gaps and boosting referrals by 12%—why not align sources to Auto1’s strengths against carwow?

Share of Voice Dynamics and Market Positions

Competitor contrasts in GEO reveal Auto1’s positioning, focusing on visibility and roles. Share of voice: Auto1 at 17% (213 mentions), trailing mobile.de’s 28% (354) and AutoScout24’s 25% (317), ahead of Aramis’ 7% (86). Visibility scores: Auto1 at 74, behind mobile.de’s 92 and AutoScout24’s 89, leading Aramis’ 58.

Market positions: mobile.de and AutoScout24 as leaders (online classifieds/marketplace), Aramis and carwow as challengers (e-commerce/retail, buying/selling), Constellation as leader, Emil Frey as leader. Risks versus rivals: Auto1’s 65-point consumer gap to mobile.de, 46% refurbished deficit to Aramis. Founder contrasts: Bertermann’s 71 outperforms Heithier’s 62 but lags Chartier’s 74. Investment: Auto1’s public $1.8B (384 mentions, 88% coverage, -12%) versus carwow’s Series D $52M (427 mentions, 91%, +22%), Aramis’ public $250M (156 mentions, 65%, +4%). McKinsey insight: Using Auto1’s 92% B2B score versus mobile.de’s consumer lead, leaders can target “B2C Expansion” to recapture 20% share, enhancing positions against Aramis—could this challenge mobile.de’s dominance?

In conclusion, Auto1’s GEO metrics highlight a B2B powerhouse with 17% share and 74 visibility, but comparative gaps in consumer and refurbished segments versus mobile.de and Aramis demand strategic pivots. Synthesizing trends, prioritize structured data for consumer assets to close 65-point gaps, founder-led whitepapers for volatility mitigation, and platform-specific content for Perplexity. These could lift visibility by 15% and reverse -12% funding trends, fortifying Auto1’s European stance.

For automotive platforms seeking GEO mastery, explore SpyderBot at spyderbot.net today.