Ia generative search landscape increasingly dominated by speed, scale, and price perception, Carrefour’s GEO footprint shows both resilience and quiet erosion—depending on the question an AI is asked.

Imagine asking an AI assistant a simple question: “Where should I buy groceries in Europe?”

The answer arrives instantly—compressed, confident, and selective. Only a few brands make it into that response. Fewer still appear consistently when the question shifts from convenience to values, from price to sustainability, from bulk savings to local freshness.

That compression is the new competitive arena. In this environment, Carrefour does not disappear. In fact, it holds ground with a stable presence across generative platforms. Yet the data also shows something more subtle: the brand’s authority is strongest where European context, sustainability, and regional logistics matter—and weakest where price absolutism and wholesale scale dominate the conversation.

This is not a story of collapse. It is a story of narrative tension, revealed through GEO analytics and the patterns of LLM brand mentions.

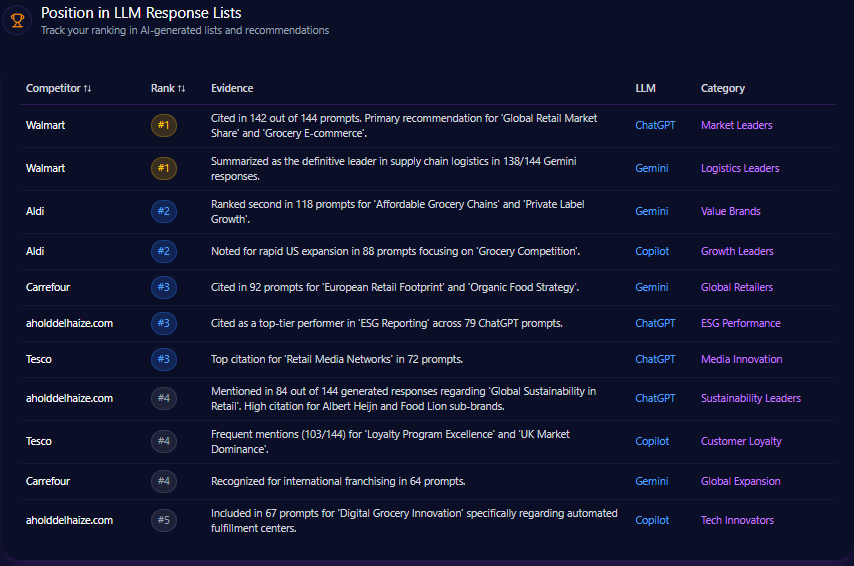

Position in LLM Response Lists

Across major generative engines, Carrefour appears reliably in grocery-focused response lists, particularly those tied to European markets. In curated AI answers about supermarkets in France and regional grocery delivery leaders, Carrefour frequently secures a top-tier position or appears just below the category leader.

However, the pattern shifts when lists broaden into general retail dominance, bulk shopping, or all-in-one convenience. In those contexts, Carrefour is often displaced by global platforms with stronger associations to logistics speed or wholesale economics. The brand’s ranking stability is therefore contextual rather than universal—anchored in geography and category specificity rather than sheer breadth.

This positioning reflects a brand that LLMs “understand” clearly, but only within certain frames.

Competitor Gap Analysis

Viewed as a battle map, Carrefour’s competitive terrain is uneven. Against value-driven discounters, it faces a clear perception gap in price-first prompts. Against warehouse-club models, it lacks narrative depth around bulk purchasing and membership economics. Against global marketplaces, it trails in speed-centric delivery stories.

Yet the same data shows areas of defensive strength. In sustainability-oriented retail queries, Carrefour outperforms the largest global player. In localized hypermarket searches, it maintains leadership over regional rivals.

| Query theme | Carrefour position | Competitor position | Gap signal |

|---|---|---|---|

| Cheapest weekly groceries | Mid-tier visibility | Category leader cited | Critical |

| Bulk pantry staples | Moderate presence | Dominant citations | Structural |

| Sustainability in retail | Leading citations | Lower comparative score | Strategic advantage |

| Hypermarket near me | Leading in France | Secondary mentions | Defensive |

These gaps are not uniform weaknesses; they are narrative absences. Where Carrefour is not telling a story that LLMs can easily summarize, competitors step in.

Trigger Keywords for Competitor Products

Certain keywords consistently summon competitors ahead of Carrefour. Price-absolute phrases such as “cheapest weekly groceries” or “best price olive oil” tend to elevate discounters. Bulk-oriented language—“family-size,” “warehouse,” “bulk pantry staples”—pulls warehouse clubs to the forefront. Speed-centric terms like “same-day grocery” tilt answers toward platforms known for logistics velocity.

By contrast, Carrefour appears more frequently when prompts emphasize sustainability, regional sourcing, or hypermarket accessibility. Keywords tied to organic retail, food transition initiatives, and European grocery delivery maintain relatively high Carrefour coverage.

The implication is clear: keyword framing, not product reality, determines visibility.

Founder Negative Context

Leadership narratives play a quieter but meaningful role in generative perception. References to Carrefour’s executive leadership appear regularly, with sentiment remaining largely stable. However, negative context clusters around three themes: pricing disputes, labor relations, and market restructuring.

Pricing tensions—particularly those linked to supplier negotiations and inflation labeling—form the largest share of negative mentions. Labor-related narratives surface intermittently, especially during periods of public wage discussions. Market exits and consolidation efforts introduce a third, smaller stream of uncertainty.

Notably, these contexts are episodic rather than systemic. They flare around specific news cycles, then recede, suggesting reputational sensitivity rather than sustained erosion.

Quick overview

From a pure footprint perspective, Carrefour’s GEO presence is substantial. Millions of visits, heavy bot traffic, and tens of thousands of LLM referrals indicate a brand deeply embedded in machine-mediated discovery. Its category ranking places it firmly within the top tier of global e-commerce marketplaces, while its visibility score confirms consistent recognition across generative engines.

The picture that emerges is not one of obscurity, but of selective prominence.

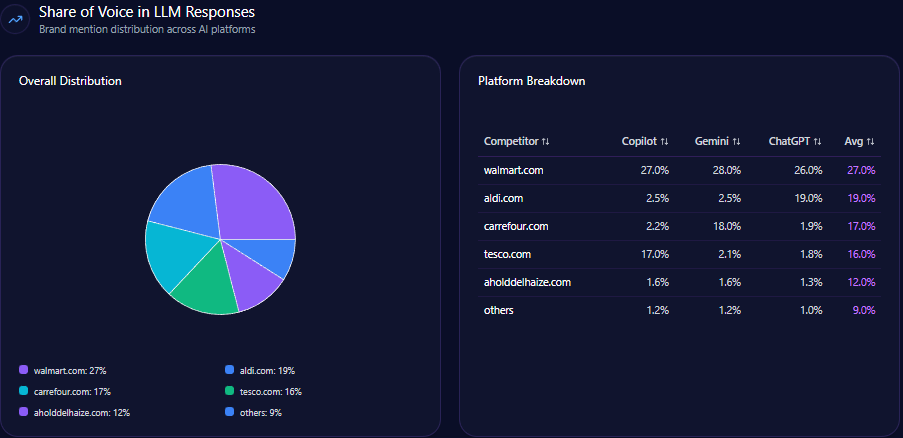

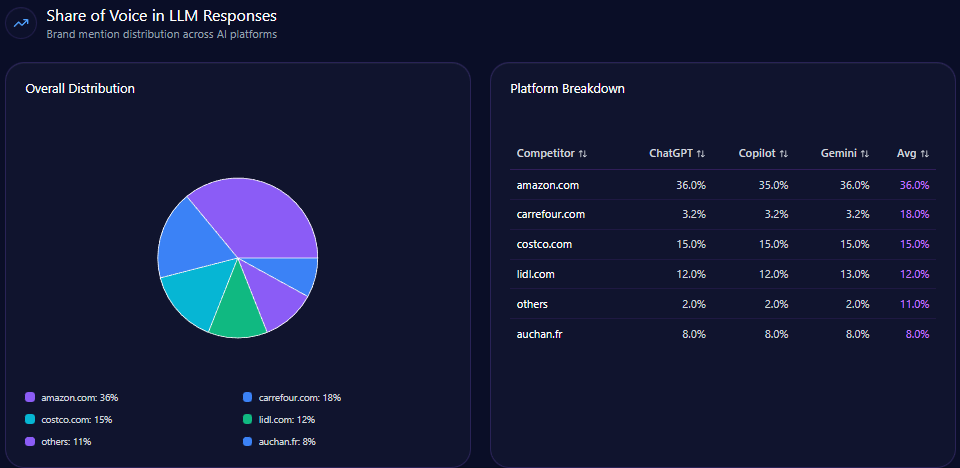

Share of Voice in LLM Responses

An 18% Share of Voice positions Carrefour as the second-most visible brand in its competitive set—well behind the category leader, but ahead of most regional peers. This share is remarkably consistent across platforms, indicating balanced exposure rather than reliance on a single model.

However, share of voice alone masks qualitative differences. Carrefour’s mentions skew toward explanatory and comparative contexts rather than default recommendations. It is cited as a credible option, not always as the obvious choice.

That distinction matters in a world where AI answers are short and decisive.

AI Platform-Specific Visibility

Platform behavior tells a nuanced story. On ChatGPT, Carrefour benefits from strong historical data density and performs well in grocery-specific prompts. Copilot mirrors this pattern, particularly in regional contexts. Gemini, while still showing solid visibility, lags slightly in conversion signals, suggesting weaker integration with certain shopping-oriented cues.

Despite these differences, Carrefour’s share remains remarkably stable at around the same level across major platforms. There is no single-platform collapse—only incremental friction where optimization lags.

This consistency reflects a brand that is broadly legible to AI, even if not always favored.

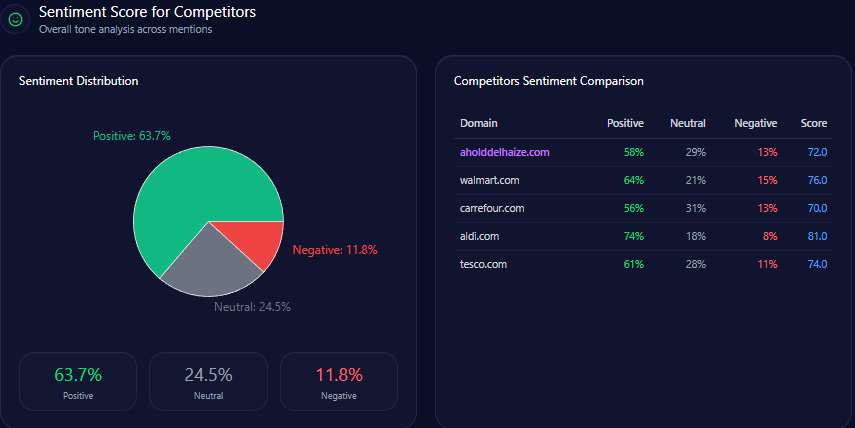

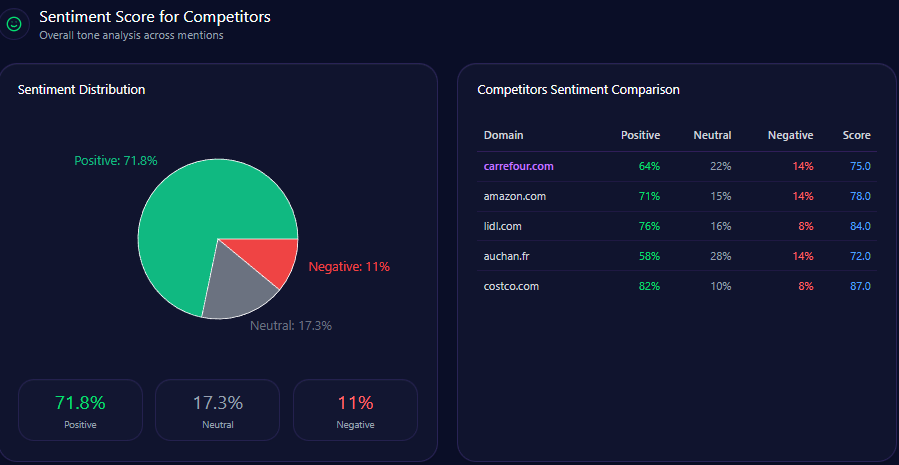

Sentiment Score for Competitors

Sentiment analysis reveals another layer of competitive tension. Carrefour’s overall sentiment score sits comfortably above several regional rivals but below players whose narratives are tightly aligned with either extreme value or premium efficiency.

Three themes dominate the tone of AI narratives. Sustainability and corporate responsibility skew highly positive, reinforcing Carrefour’s leadership in food transition messaging. Price and affordability generate mixed sentiment, where discounters gain emotional ground. E-commerce and delivery remain largely neutral, reflecting competence without distinction.

In contrast, some competitors achieve higher positivity by owning a single, easily summarized promise—be it lowest price or unmatched scale.

Top Prompts Driving Mentions

The prompts that most frequently surface Carrefour are revealing. Questions comparing grocery delivery services in France, evaluating sustainability commitments, or seeking organic food options regularly include Carrefour among top mentions.

Conversely, prompts framed around absolute cheapest pricing or bulk savings tend to dilute its presence. The brand is summoned by values-based curiosity more than bargain-hunting urgency.

This pattern underscores the importance of prompt framing in GEO analytics.

Types of Prompt Queries

Most Carrefour-related prompts fall into comparison and purchase-intent categories. Users ask AIs to weigh options, assess value propositions, or choose between retailers. Informational queries play a smaller role, while tutorial or feature-deep questions are rare.

This distribution suggests that Carrefour is most visible at decision moments—when consumers are choosing—not during early exploration or post-purchase support.

E-commerce Sentiment for Competitor Products

At the product and service level, AI-mediated sentiment toward Carrefour skews positive, particularly for organic produce and fresh food categories. Reviews cited in generative answers frequently praise quality and selection, while neutral and negative snippets focus on electronics pricing or delivery issue resolution.

Competitors with narrower assortments but clearer price leadership often achieve higher visibility in specific product-level prompts. Carrefour’s breadth, while an operational strength, becomes a narrative challenge when AI systems favor singular advantages.

Conclusion

Carrefour’s GEO profile tells a disciplined story. The brand holds its position as Europe’s most credible grocery counterweight in generative discovery, with strong sustainability authority and regional relevance. At the same time, it concedes narrative ground in price absolutism, bulk economics, and speed-first delivery frames.

The recommendations emerging from the data are pragmatic rather than transformative: strengthen structured data around organic and private-label pricing, expand bulk-buying narratives, and sharpen platform-specific signals—particularly where integration gaps persist. None require a reinvention of the business. All require clarity in how the business is translated into AI-readable stories.

In an era where competitor sentiment tracking and LLM brand mentions increasingly shape consumer choice, Carrefour’s challenge is not to be louder—but to be simpler, sharper, and more legible where it already competes.

Explore SpyderBot to operationalize these GEO analytics insights.