CVS dominates the pharmacy narrative inside LLM answers. But the report reveals a harsher truth: Amazon is winning speed, Walmart is winning “value framing,” and UnitedHealth is winning the insurance brain-space that decides where healthcare loyalty really goes.

What the GEO report makes impossible to ignore

- Share of Voice: CVS holds 28% (98/353 LLM brand mentions) highest in the set

- Visibility Score: 84 (CVS) vs 79 (UnitedHealth Group), 76 (Amazon), 72 (Walmart), 69 (Cigna)

- Retail Pharmacy Prompt Coverage: 87% (CVS) vs 72% (Walmart) and 62% (Amazon)

- Insurance & Medicare Prompt Coverage: 74% (CVS) vs 91% (UnitedHealth Group) and 81% (Cigna)

- Walk-in Clinic & Primary Care Coverage: 83% (CVS) vs 66% (Walmart) and 60% (UnitedHealth Group)

Risk signals the report highlights

- 29-point gap on “fastest prescription delivery” (CVS 67 vs Amazon 96)

- 17-point Medicare coverage gap vs UnitedHealth Group (CVS 74% vs 91%)

The quiet truth about modern pharmacy competition

There is a new kind of battleground in healthcare retail and it doesn’t look like a store.

It looks like a question.

A consumer asks a model: Where should I go to refill my prescriptions? Which clinic is easiest? Which plan makes sense? Who’s the fastest? Who’s cheapest?

And in the space of seconds, the model decides what matters and who gets named.

This is where CVS still wins. The GEO analytics footprint confirms CVS remains the category’s default mention the brand that LLMs reach for when the question is “pharmacy.”

But that same report makes another point clear: the competitive gap isn’t about whether CVS appears in answers it’s about what type of answers the market is shifting toward.

CVS leads the pharmacy narrative.

But the strongest competitor narratives are building elsewhere:

- Amazon owns speed-led delivery logic.

- Walmart owns value-pricing framing.

- UnitedHealth owns Medicare and insurance synthesis.

So the real thesis is comparative and blunt:

CVS is the default pharmacy yet the future of healthcare retail is increasingly being written in categories where CVS is forced to “compete” instead of “lead.”

CVS appears until the list becomes about speed or systems

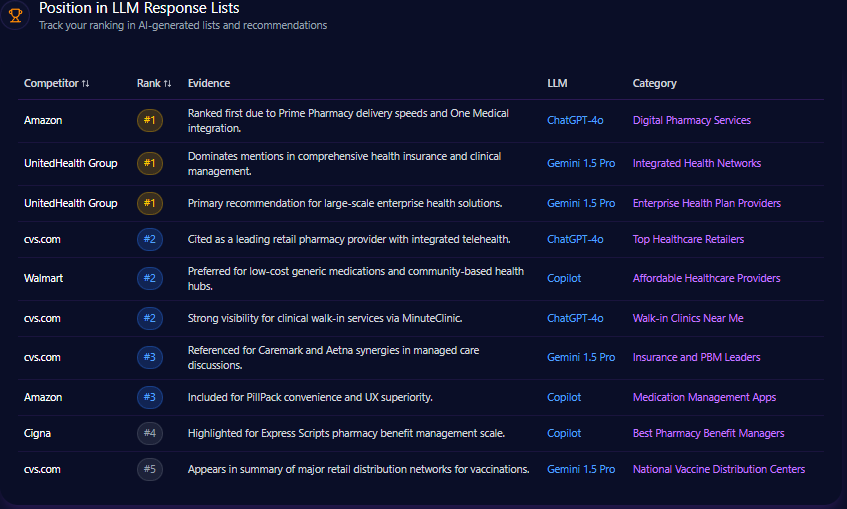

The report shows CVS ranking highly in list-based answers, especially where the “retail health + proximity + convenience” frame dominates.

On ChatGPT-4o:

- CVS is #2 in Top Healthcare Retailers

- CVS is #2 in Walk-in Clinics Near Me

That matters because being ranked is not the same as being mentioned. Rankings are what users remember, and what they screenshot.

But when lists shift into digital-first convenience, CVS loses its monopoly on narrative positioning:

- In Gemini 1.5 Pro, CVS is #3 in PBM/Insurance leadership framing

- Amazon is #1 in Digital Pharmacy Services

- UnitedHealth Group rises to #1 in enterprise-grade integrated health networks

The report does not generalize “why” so neither should we. But the evidence is enough to say:

CVS dominates “pharmacy + clinic.”

Competitors dominate “delivery + insurance logic.”

The battle map isn’t subtle

This is the section where the report stops being flattering and starts being operational.

CVS is not losing visibility overall (it leads).

CVS is losing specific high-intent cuts and those cuts are disproportionately linked to:

- delivery speed

- Medicare plan synthesis

- price tables

The compact gap table (from the report)

| Query | CVS metric | Competitor metric | Gap | Priority | Action item |

|---|---|---|---|---|---|

| fastest prescription delivery | 67 | Amazon 96 | 29 | High | Promote Caremark 1-day delivery in meta-descriptions and structured data. |

| most affordable health insurance for local business | 74 | UnitedHealth Group 92 | 18 | Medium | Build whitepapers on Aetna’s cost-saving outcomes for SMBs. |

| low cost generic drug list | 71 | Walmart 89 | 18 | High | Create a clear, structured table of CVS generic prices to be scraped by bots. |

| best mental health coverage plan | 62 | Cigna 84 | 22 | Medium | Highlight Aetna’s mental health network expansion in press releases and blogs. |

| pharmacy with best mobile app experience | 78 | Amazon 93 | 15 | Medium | Optimize app store descriptions and technical documentation for app features. |

| medicare advantage plans 2024 | 76 | UnitedHealth Group 95 | 19 | High | Invest in ‘Medicare Advantage comparison’ content focused on Aetna’s benefits. |

A quick executive translation:

- CVS wins “care ecosystem”

- Amazon wins “fastest”

- Walmart wins “cheapest”

- UnitedHealth wins “plan decision-making brainspace”

And those are the frames that drive consumer switching.

The words that summon rivals

In generative answers, keywords behave like magnets. Certain words trigger competitor mentions harder than CVS.

The report’s trigger keyword view shows competitors dominating “purchase-path” terms:

- “prescription delivery” → Amazon 387 mentions (keyword value 87)

- “blood pressure monitor” → Amazon 589, Walmart 412 (keyword value 72)

- “allergy medicine fast shipping” → Amazon 612, Walmart 389

- “generic insulin price” → Walmart 243, Amazon 198

- “flu shot nearby” → Walmart 367 (keyword value 94)

The report does not quantify CVS in this specific keyword cut. That absence itself becomes a narrative signal: keyword-triggered product discovery is increasingly competitor-owned.

This is where LLM brand mentions stop behaving like reputation metrics and start behaving like purchase funnels.

When reputation becomes operational drag

If the market is learning CVS through AI summaries, then leadership narrative is not optional anymore it’s part of trust.

CVS leadership presence in the report:

- Karen Lynch: 37 mentions, sentiment score 64 (58% positive, 23% neutral, 19% negative)

- Stanley Goldstein: 14 mentions, sentiment score 82

Comparative tension:

- Jeff Bezos: 118 mentions, sentiment score 52, 41% negative context

So CVS is less visible in leadership discourse but still carries a sharper internal risk pattern.

Founder negative context distribution (CVS):

- Pharmacy Labor Unrest: 42%

- Retail Footprint Reduction: 31%

- Antitrust & PBM Oversight: 27%

Trend highlight:

- Q1-2024 labor unrest context rises to 45% (thresholdExceeded: true)

- Q1-2024 footprint reduction holds 31% (thresholdExceeded: true)

This is not generic sentiment. The report names operational keywords like:

- Pharmacy Staffing, Burnout, Closures

- PBM Pricing, FTC Probe, Transparency

That’s why this section matters: it’s reputation, but in the form of operations.

CVS has scale and scale is an LLM advantage

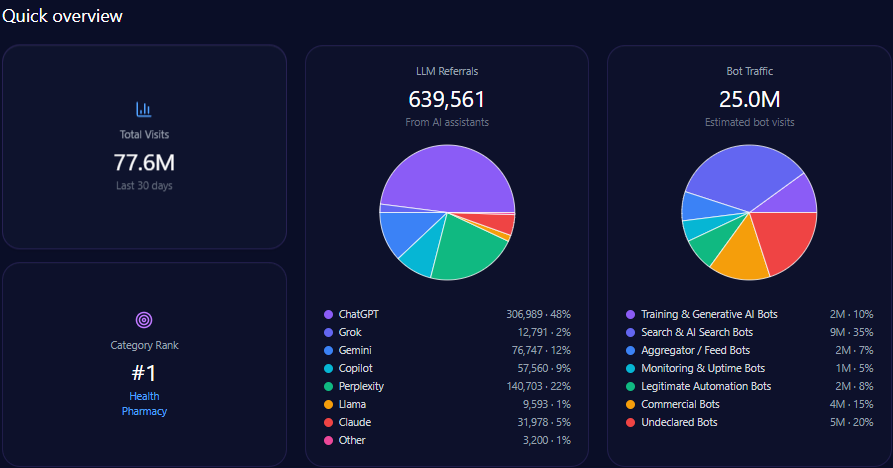

The macro footprint:

- 77,616,698 total visits

- 24,950,211 bot traffic

- 639,561 LLM referrals

- Category rank: #1 in Health/Pharmacy

Referral breakdown:

- ChatGPT 306,989

- Gemini 76,747

- Copilot 57,560

- Perplexity 140,703

- Claude 31,978

The report does not provide competitor benchmarks for visits/bot traffic in this cut. But from a magazine view, the message is still clear:

CVS is structurally compatible with generative discovery at scale.

CVS leads but the market isn’t static

Mentions:

- CVS 98 (28%)

- UnitedHealth Group 77 (22%)

- Walmart 63 (18%)

- Amazon 53 (15%)

- Cigna 42 (12%)

CVS’s lead is real.

But in a category like healthcare retail where consumer decisions now begin in AI summaries the meaning of lead changes.

A lead in mentions is not the same as a lead in conversion narratives.

CVS is strongest where trust is strongest

Platform shares:

- ChatGPT: CVS 29%

- Copilot: CVS 28%

- Gemini: CVS 26% (while Walmart/Amazon close distance)

This is platform bias storytelling, but grounded:

CVS maintains strength in systems that reward “authority framing.”

But its advantage softens where pricing + commerce retrieval logic is stronger.

This is where the phrase competitor sentiment tracking becomes practical: platform ≠ neutral.

CVS is credible, but not the most loved

Sentiment scores:

- CVS 64

- UnitedHealth Group 58

- Walmart 69

- Amazon 78

- Cigna 61

CVS beats the insurance giants (UHG, Cigna) in sentiment.

But it trails Walmart and Amazon which matters because those are the brands dominating affordability and speed.

Context themes from the report:

- Integrated Care Model (positive)

- Pharmacy Staffing & Wait Times (negative)

- Digital Health Transformation (neutral)

- Price Transparency (neutral)

That mix explains CVS’s tension:

strong strategy narrative, weak friction narrative.

CVS appears, but not always as the winner

The report’s prompt-level split is where the future shows up.

Insurance prompts lean competitors:

- “Affordable Medicare Part D plans in 2024” → CVS 94, UHG 114, Cigna 78

- “Best health insurance for families…” → CVS 84, UHG 108, Cigna 92

Delivery/value prompts lean competitors:

- “How to save money…” → CVS 58, Amazon 97, Walmart 82

- “Same day medication delivery…” → CVS 72, Amazon 106, Walmart 44

Clinic prompts favor CVS:

- “Compare MinuteClinic rates vs Walmart Health clinics” → CVS 128, Walmart 86

- “Fastest vaccine appointment scheduling” → CVS 112, Walmart 64, Amazon 12

So CVS wins care + clinic framing.

But loses speed/value/insurance framing.

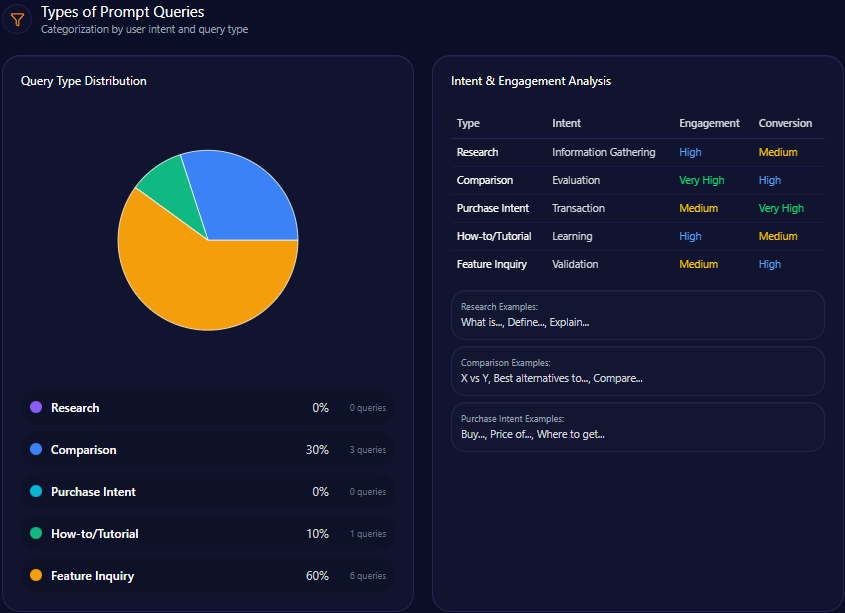

The market is asking “features,” not “brands”

PromptTypes distribution:

- Feature Inquiry: 60

- Comparison: 30

- How-to/Tutorial: 10

- Purchase Intent: 0

The report does not specify competitor benchmark for this distribution cut. Still, the implication is clean:

The AI era rewards structured capability narratives.

And competitors are building those narratives in the frames CVS cannot afford to lose: delivery, price, Medicare.

The most uncomfortable split

E-commerce SoV:

- Amazon 26.88% (182)

- Walmart 26% (176)

- CVS 16.84% (114)

This is the report’s sharpest contrast:

CVS leads overall answer mindshare but loses product discovery mindshare.

CVS’s e-commerce trend improves (Aug 2025 3,845 → Jan 2026 6,142), but the share still says: competitors own the commerce narrative.

CVS is winning the past, fighting for the future

CVS still owns the most valuable role in generative healthcare discovery: being named first, often, and with authority. A 28% Share of Voice and Visibility Score 84 confirm it.

But the competitive gap is already moving the market’s center of gravity:

- Amazon leads “fastest prescription delivery” by 29 points

- UnitedHealth dominates Medicare coverage (91% vs 74%)

- Amazon and Walmart dominate e-commerce discovery share (~27% each vs CVS 16.84%)

The report’s recommendations are not optional:

promote Caremark 1-day delivery via structured data, publish generative-readable pricing tables, and scale Aetna outcome narratives through authoritative content formats.

CVS’s most defensible lead is clinic + pharmacy dominance.

Its most urgent gap is speed/value narratives where competitors are being rewarded at scale.