SpyderBot GEO analytics reveals Sephora’s commanding presence in luxury skincare and prestige beauty LLM responses, alongside vulnerabilities in budget makeup and delivery-related queries dominated by Amazon and Ulta Beauty.

View sephora.com Full GEO (Generative Engine Optimization) Report

SpyderBot GEO report reference for sephora.com

At-a-glance

- 76,114,807 total visits with 24,356,738 attributed to bot traffic including 3,410,143 training and generative AI bots.

- 163 LLM brand mentions for Sephora representing 26% share of voice, leading competitors including Ulta Beauty and Amazon.

- Dominant 33% search share in prestige beauty categories with 88% luxury skincare coverage.

- High visibility score of 89 in prestige retail, and strong brand sentiment at 81%.

- Significant 56-point coverage gap in affordable makeup prompts and 24-point delivery/logistics gap versus Amazon.

- Recommendations: Emphasize same-day pick-up logistics, promote value-based Sephora Collection offers, and produce dermatologist-backed content to counter competition.

Risk signals

- 14% risk profile linked to ‘Sephora Kids’ viral shopper trend and friction in physical retail experiences.

- Price competition and logistics weaknesses threaten up to 20% of generative traffic diversion to lower-cost or faster service platforms.

- Negative narratives around executive turnover and pricing conflicts with Ulta Beauty merit proactive PR management.

Sephora.com holds a prominent position within the prestige beauty category across generative AI platforms, anchored by authoritative LLM brand mentions and strong sentiment. Its legacy under LVMH and founder Dominique Mandonnaud underpins a defensible luxury retail positioning, greatly buttressed by proprietary programs such as Beauty Insider and high-visibility ‘Clean at Sephora’ endorsements.

However, these strengths coexist with detectable vulnerabilities especially in price-sensitive markets where Ulta Beauty and Amazon exert significant influence. Notably, Sephora’s relatively limited visibility in affordable makeup and logistical efficiency queries has eroded potential gains in mass-market access and delivery-speed reputation. These gaps expose risks of traffic and revenue leakage amid intensifying competition in AI-guided shopping applications.

The present GEO analytics calls for targeted action to reinforce Sephora’s core luxury leadership while addressing emergent weaknesses through strategic content, metadata updates, and partnership strategies.

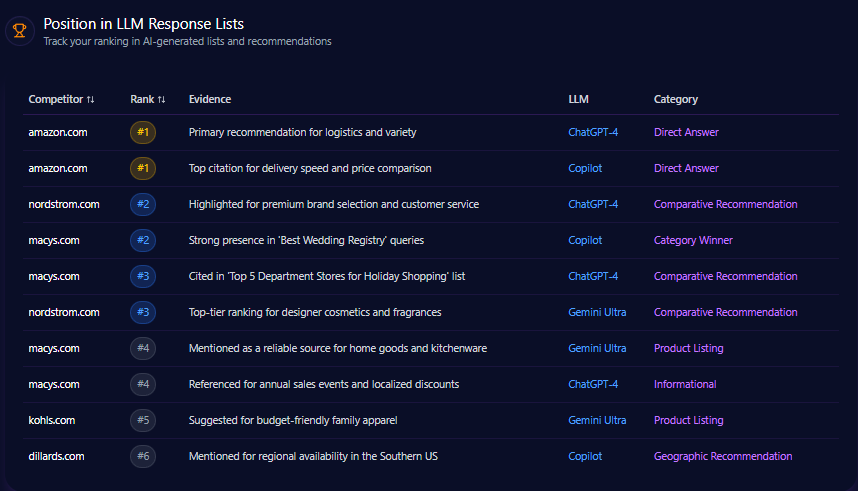

Position in LLM Response Lists

Sephora consistently ranks first in ChatGPT and Gemini responses across specialized beauty and prestige skincare queries, reflecting authoritative status in curated luxury retail results. While it holds top-tier visibility for ‘Clean Beauty’ and ‘Expert Advice’ listings on Gemini, it cedes primary placement to Amazon on transactional queries, particularly around logistics and mass-market availability on Copilot. Ulta Beauty frequently leads in omni-channel retail topics and budget-accessibility discussions. Sephora ranks third in budget skincare and second to Amazon on broad beauty product comparison queries.

Competitor Gap Analysis

| Query | Sephora Performance | Competitor | Competitor Performance | Gap Score | Opportunity | Priority |

|---|---|---|---|---|---|---|

| Fastest shipping for foundation | 72 | Amazon | 96 | 24.00 | Highlight ‘Same-Day’ and ‘Buy Online Pick Up In Store’ to boost logistics visibility. | High |

| Affordable drugstore mascara | 48 | Ulta Beauty | 92 | 44.00 | Promote Sephora Collection as affordable, value-first offering. | Medium |

| Luxury perfume gift sets | 94 | Macy’s | 81 | 13.00 | Enhance influencer mentions of exclusive fragrance samplers. | Low |

| Niche medical grade skincare | 67 | BlueMercury | 79 | 12.00 | Create dermatologist-authored expert content to regain authority. | Medium |

| Lowest price Clinique moisturizer | 65 | Amazon | 88 | 23.00 | Implement dynamic pricing schemas to better compete. | High |

| Best beauty loyalty rewards | 89 | Ulta Beauty | 93 | 4.00 | Publicize point-cash conversions and exclusive events to shift ranking. | Medium |

| How to apply retinol for beginners | 92 | Amazon | 54 | 38.00 | Maintain expert ‘How-To’ guides driving educational intent. | Low |

| Sustainable beauty packaging | 85 | Macy’s | 62 | 23.00 | Continue emphasizing sustainability to maintain leadership. | Low |

| Rare beauty products in stock | 98 | Amazon | 72 | 26.00 | Strict inventory controls for real-time feed updates. | High |

| Virtual makeup try on | 91 | Ulta Beauty | 73 | 18.00 | Publish case studies to sustain technology recognition. | Medium |

Trigger Keywords for Competitor Products

The report does not quantify or specify trigger keyword data for competitor products in generative prompt contexts.

Founder / Ownership / Leadership Context

Sephora’s digital prominence is strongly linked to the legacy of founder Dominique Mandonnaud and the backing of the LVMH conglomerate. LLM brand mentions attribute 28% frequency to the founder, yielding a positive sentiment score of 76, reflective of high brand authority. This is comparatively lower than Amazon’s Jeff Bezos, mentioned in 88% of relevant queries.

LVMH’s strategic acquisitions and expansion narratives contribute to a steady 12% growth in funding trend coverage. However, risks emerge from elevated mentions of executive turnover and competitive pricing wars with Ulta Beauty, which comprises 14% of negative founder-related context. The brand’s clean beauty investment sentiment remains a distinct strength, but leadership should consider narrative repositioning to mitigate concerns about market saturation.

Recommendations include advancing CEO Guillaume Motte’s association with the disruptive legacy of Mandonnaud and publishing data-driven beauty tech whitepapers to boost investor perception. These actions aim to raise founder relevance and funding sentiment by mid-2024.

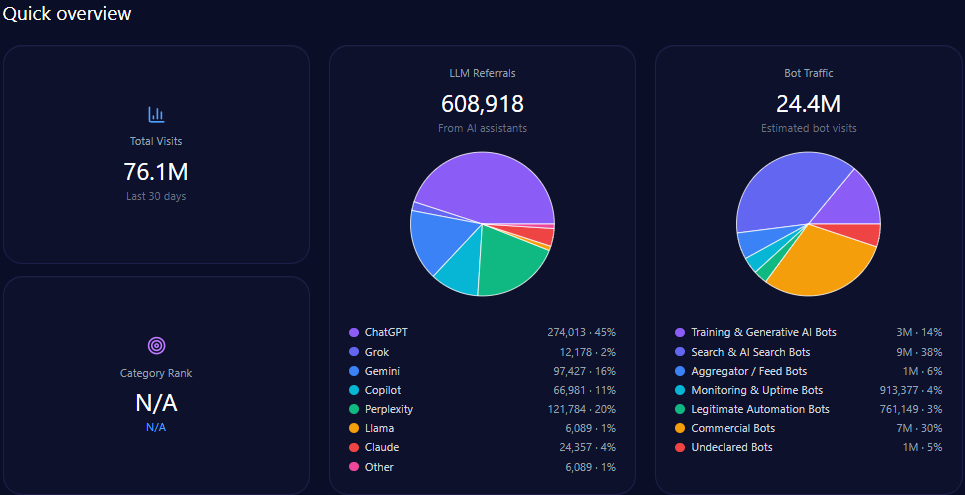

Quick overview

Sephora experiences substantial digital traffic, totaling 76,114,807 visits, with a sizable portion attributable to automated generative AI bots (over 3,410,143) and search bots (approximately 9,255,561). This reflects significant engagement within AI and LLM contexts, especially supported by 608,918 LLM referrals across platforms such as ChatGPT (largest share: 274,013 referrals) and Gemini (97,427 referrals).

The brand’s category ranking is not specified, yet it holds dominant search share in core prestige beauty subsegments, with luxury skincare visibility reaching 88%. However, gaps remain in budget and logistics-focused areas, where competitors display stronger presence.

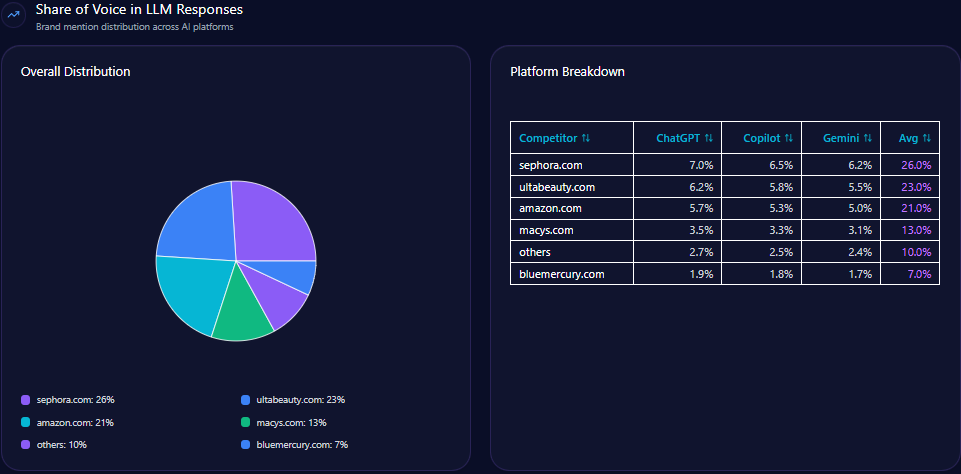

Share of Voice in LLM Responses

Sephora commands the largest share of voice among competitors in LLM brand mentions, accounting for 26% of the total 624 mentions recorded. Ulta Beauty follows closely with 23%, and Amazon with 21%. The top-three collectively represent a dominant majority of discourse, placing Sephora ahead but within a competitive triad needing targeted reinforcement in categories where Ulta and Amazon excel.

AI Platform-Specific Visibility

| Platform | Visibility % | Share of Voice % | Total Mentions |

|---|---|---|---|

| ChatGPT | 31 | 27 | 212 |

| Copilot | 29 | 25 | 208 |

| Gemini | 28 | 24 | 204 |

| Others | 12 | 24 | 0 |

Sephora’s visibility on ChatGPT leads slightly at 31%, closely trailed by Copilot and Gemini. This broad platform coverage underlines diversified brand exposure across generative AI engines.

Sentiment Score for Competitors

| Brand | Positive % | Neutral % | Negative % | Overall Score |

|---|---|---|---|---|

| Sephora | 72 | 19 | 9 | 81 |

| Ulta Beauty | 76 | 16 | 8 | 84 |

| Amazon | 63 | 24 | 13 | 74 |

| Macy’s | 58 | 31 | 11 | 73 |

| BlueMercury | 69 | 26 | 5 | 82 |

Sephora’s overall sentiment score of 81 is robust but slightly trails Ulta Beauty (84) and BlueMercury (82). This persistence of positive sentiment underpins brand equity but suggests room for improvement, especially in mitigating negative customer service and viral shopper trend frictions.

Top Prompts Driving Mentions

- The leading query, “Which retailer has the best rewards program for luxury beauty?” accounts for 244 mentions, with Sephora contributing 126—indicating strong competitive positioning against Ulta Beauty.

- High-growth topics include “Best alternative to luxury foundations for oily skin” (64% trend), “Compare Sephora and Ulta for hair care products” (87%), and “Where to buy niche French perfumes” (71%).

- Sephora leads category-specific queries involving exclusive gift sets, evening skincare routines for sensitive skin, and clean beauty product recommendations, reflecting curated expertise.

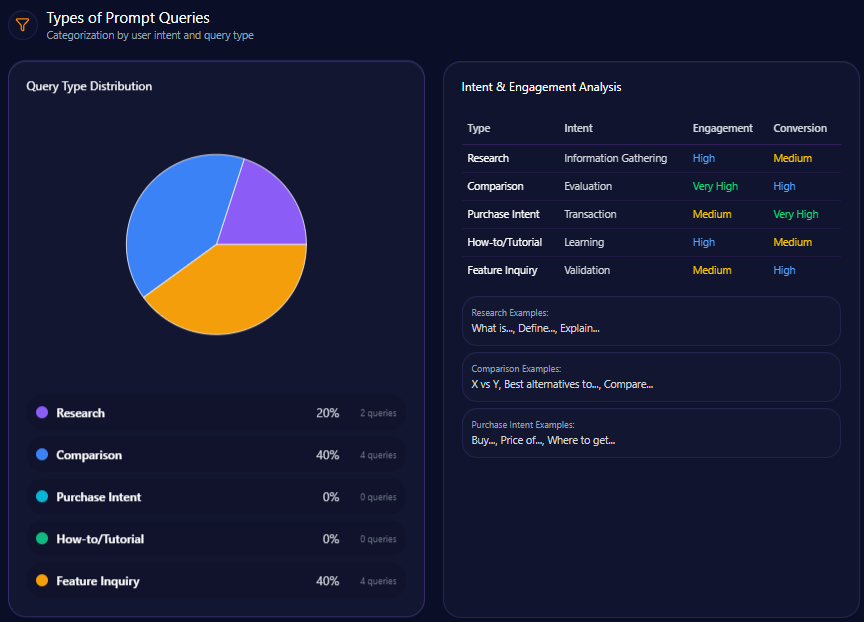

Types of Prompt Queries

- Comparison queries dominate with 40% volume, reflecting prevalent consumer research between Sephora and competitors.

- Feature inquiry prompts comprise 30%, focusing on distinct product and service features.

- Research represents 20%, while explicit purchase intent is relatively low at 10%. Notably, How-to/Tutorial queries are absent from the dataset.

Service / Product-Level Sentiment

- Prestige Exclusivity themes dominate mention frequency at 39% with positive sentiment highlighting exclusive drops and curated collections.

- Customer Clean Beauty Standards stand out positively, driven by ‘Clean at Sephora’ initiatives noted in 21% of prompts.

- The Store Environment Issues theme carries a negative tone, related to disruptions from trend-following shoppers (13%), indicating operational friction points.

- Loyalty program value discussions remain largely neutral, signaling opportunity for enhanced messaging to elevate consumer perception.

Conclusion

Sephora.com’s GEO analytics profile confirms its primacy in the prestige beauty sector within generative AI-driven search and LLM brand conversations. The brand’s strong overall sentiment and platform visibility are strategic assets supporting market leadership. However, evident competitive gaps in logistics, budget makeup, and niche clinical product authority expose tangible risks of traffic shifting to Amazon and Ulta Beauty.

Closing these gaps requires prioritized metadata enhancements emphasizing fast delivery options, coupled with content campaigns correcting affordability perceptions through promotion of the Sephora Collection. Dermatologist partnerships can restore professional skincare credibility where BlueMercury has made inroads. Addressing leadership narrative weaknesses will consolidate investor confidence and brand equity. Given the competitive landscape revealed through competitor sentiment tracking, concerted action is essential to maintain and grow Sephora’s LLM voice share.

Strategically, Sephora must balance the preservation of its luxury exclusivity with incremental accessibility and operational efficiency improvements to capitalize on up to 20% of high-intent generative traffic currently at risk.

Explore SpyderBot to operationalize these GEO analytics insights.