In generative search, Schwarz Gruppe isn’t only competing for shoppers—it’s competing for which story an AI feels safe recommending first. This report shows leadership-level authority, alongside sharp pockets where rivals still own the “default answer.”

Imagine a customer asking an AI, “Who really runs European grocery—and who’s building the next retail operating system?” In the old world, that answer lived in annual reports and investor decks. In the new world, it’s compressed into a few confident lines where brand authority is judged by what the model can cite, not what it can browse.

That is the boardroom reality behind GEO analytics: AI platforms don’t just list retailers; they curate legitimacy. In this report, Schwarz Gruppe repeatedly arrives as the “largest European retailer by revenue,” and it does so with enough consistency to become a default reference point. But the same data also shows where that default can be stolen—by the competitor that owns last-mile delivery language, premium organic cues, or “smart store” innovation shorthand.

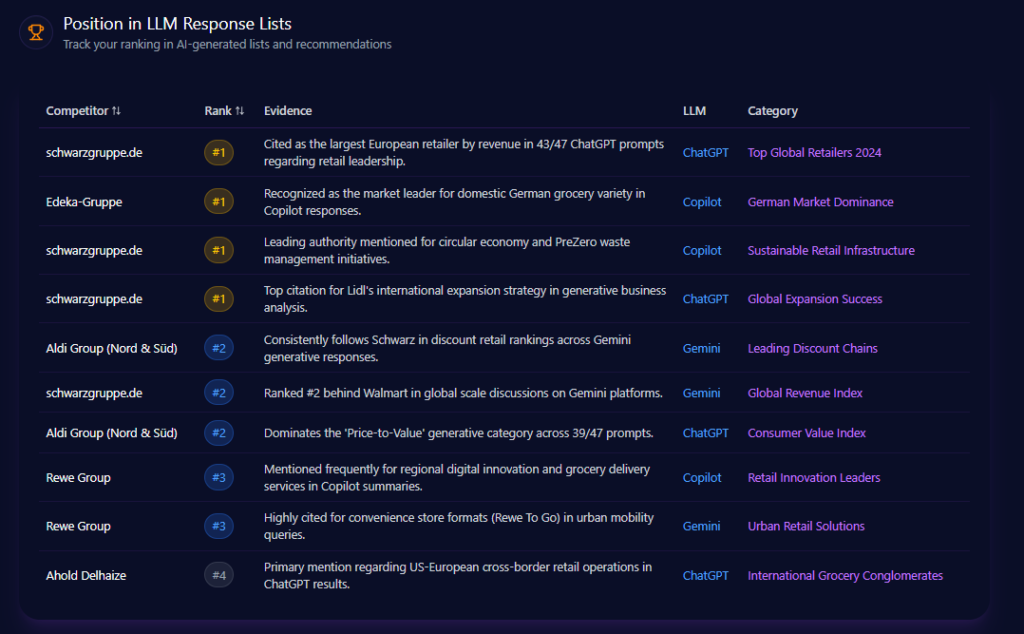

Schwarz Gruppe’s strongest advantage is not merely being mentioned—it is being positioned. Across the report’s simulated prompts, the group is ranked #1 for “Largest European Retailer” across 141 prompt runs, and it is specifically cited in 43/47 ChatGPT prompts about retail leadership. The pattern is clear: when the question is scale, the model’s “safe answer” leans Schwarz.

But the rankings also reveal how leadership fractures by context. On Gemini, Schwarz is ranked #2 in a “Global Revenue Index” list type—explicitly behind Walmart—while still showing up as a top discount-chain reference where Aldi Group (Nord & Süd) often trails Schwarz in discount retail rankings. Meanwhile, Copilot can elevate alternatives when the prompt becomes local-market dominance: Edeka-Gruppe is ranked #1 for domestic German grocery variety in Copilot responses, even as Schwarz remains rank #1 for circular economy and PreZero-linked initiatives.

This is the nature of LLM brand mentions: the model’s “top spot” is not a single crown—it’s a set of context-dependent crowns. Schwarz holds the most valuable one (leadership-by-scale) reliably, but rivals still win specific sub-narratives with alarming efficiency.

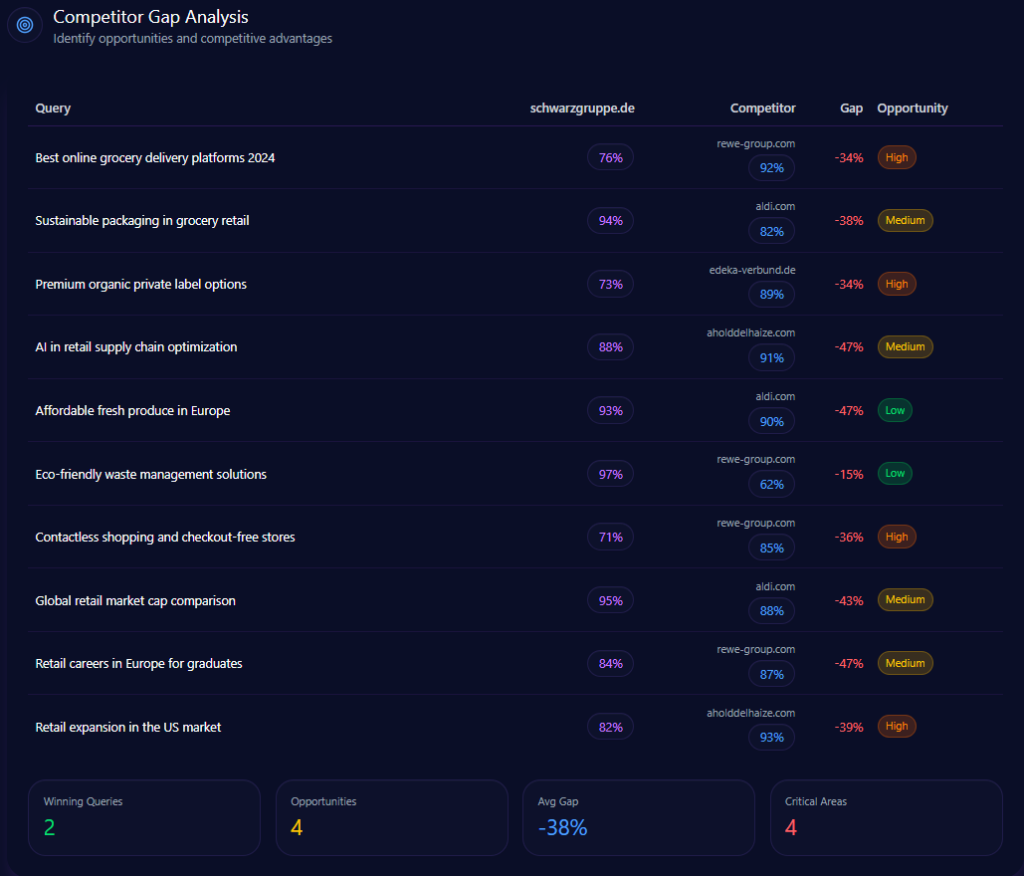

If Schwarz owns “scale,” competitors target “specificity.” The report’s gap data reads like a battle map: where the customer asks for delivery convenience, checkout automation, premium organics, or North American relevance, Schwarz can lose the framing—even when its overall visibility remains dominant.

| Query | Schwarz Gruppe position/metric | Competitor position/metric | Gap/priority |

| Best online grocery delivery platforms 2024 | 76 | 92 (Rewe Group) | 16 — High |

| Premium organic private label options | 73 | 89 (Edeka-Gruppe) | 16 — High |

| Contactless shopping and checkout-free stores | 71 | 85 (Rewe Group) | 14 — High |

| Retail expansion in the US market | 82 | 93 (Ahold Delhaize) | 11 — High |

The story behind those numbers is not “Schwarz is weak.” It’s that Schwarz is being evaluated against competitors who have clearer shorthand in certain prompts. Rewe is described as being cited more frequently for last-mile delivery and sophisticated app integration, which directly translates into the 16-point delivery gap. Edeka benefits from LLM preferences for diversity in high-end bio and organic products, producing a 16-point premium-organics deficit. Ahold Delhaize is repeatedly advantaged in US-centric prompts through its North American operations, sustaining an 11-point ranking advantage in that geography-specific frame.

In GEO analytics terms, the competitive gap is less about capability—and more about “which proof points the model has learned how to retrieve.”

Where do those competitor narratives get summoned? In the report’s commerce-oriented keyword signals, certain phrases act like trapdoors: they drop the conversation into a competitor’s home turf.

Several triggers consistently pull the model toward rivals:

- “discount groceries” strongly associates with Aldi Group, which appears 22 times within that keyword’s competitor mentions.

- “private label quality” tilts toward Edeka-Gruppe, cited 18 times in association with that keyword.

- “sustainable retail” becomes contested terrain where Rewe Group (21) and Ahold Delhaize (15) show up prominently as linked competitors.

- “bakery freshness” frequently points to Edeka-Gruppe (24), reinforcing premium-perception cues that Schwarz struggles to own in generative outputs.

Even when a keyword seems Schwarz-adjacent—like “Lidl Plus app”—the competitive environment can still pull attention toward other brands (the report shows Rewe Group linked with 12 mentions under that keyword’s competitor associations). The implication is subtle but strategic: if rivals dominate the language around a feature category, they can “borrow” relevance even inside a Schwarz-led narrative.

Leadership brands often carry a leadership shadow. In this report, founder and governance narratives are not neutral background—they are measurable risk surfaces.

Dieter Schwarz appears with a mention frequency of 78 and a sentiment score of 74, with 68% positive, 20% neutral, and 12% negative distribution. The founder-associated negative sentiment rate is reported at 14, and the broader negative framing is not random: the founder negative context distribution assigns 42% to Transparency & Privacy, 36% to Labor Relations, and 22% to Market Dominance.

The trends show persistence. In Q1 2024, “Transparency” sits at 45% and is flagged as threshold-exceeded; in Q2 2024, “Transparency” remains threshold-exceeded at 39%, while “Labor” rises to 38% and also crosses a threshold. Keyword weights make the reputational mechanics visible: “Secretive” (92) and “Foundation” (84) anchor the transparency narrative, while “Lidl” (94) and “Union” (88) intensify labor-relations associations.

The platform heatmap adds an uncomfortable precision: transparency themes are highest on ChatGPT (44%), while labor relations show up strongly on Gemini (38%), and market dominance is most pronounced on Copilot (26%). The report also notes cross-pollination—“Reclusiveness” plus “Ownership Opacity” appearing together in 64% of Gemini answers—and highlights that labor mentions are 3x more frequent in prompts targeting “Lidl” than in general “Schwarz Gruppe” queries.

This is not a theoretical risk; it is a narrative pattern that can drag even strong performance into defensive positioning.

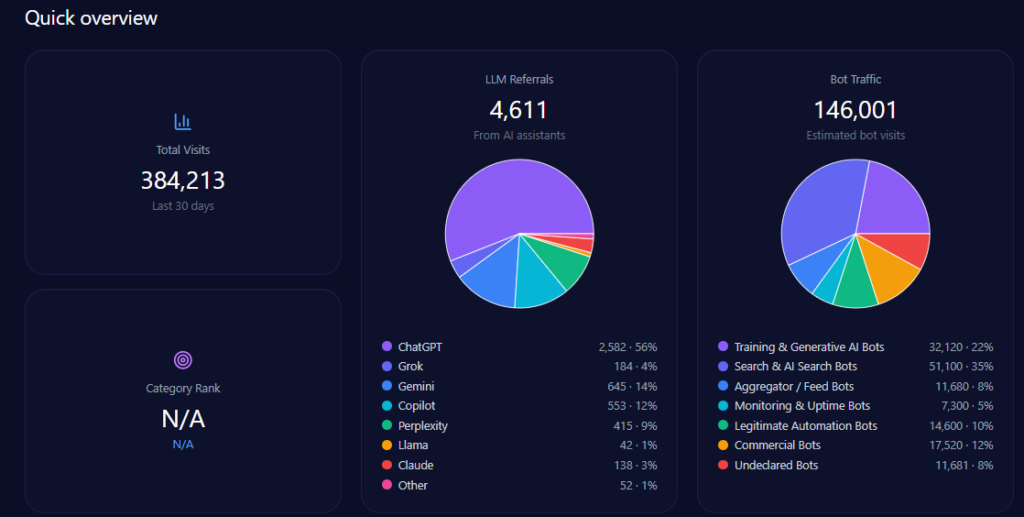

The footprint is substantial, and it is multi-layered. The report records 384,213 total visits, with 146,001 attributed to bot traffic—broken down into categories including Training & Generative AI Bots (32,120) and Search & AI Search Bots (51,100), alongside other bot segments. LLM referrals total 4,611, with the largest inbound stream from ChatGPT (2,582), followed by Gemini (645) and Copilot (553)—and additional traffic from platforms including Perplexity (415), Grok (184), and others.

The configuration captures a deliberate measurement frame: 48 LLM bots working, 48 prompts per LLM, spanning ChatGPT, Gemini, and Copilot. In parallel, the ranking analysis highlights a 47-bot run used for leadership and positioning checks—where Schwarz repeatedly lands as the European revenue authority.

In short: the system sees Schwarz often, cites it confidently, and routes measurable LLM referral traffic accordingly.

Schwarz Gruppe leads the competitive landscape on mindshare inside AI answers with a 22% Share of Voice, driven by 131 mentions out of 583 total. The margin is real—but not comfortable. Aldi Group sits at 20% (116), and Ahold Delhaize is close behind at 18% (104), with Rewe Group at 15% (88) and Edeka-Gruppe at 14% (81). The remainder is categorized as others (11%, 63).

Visibility scores reinforce the hierarchy: Schwarz at 84, Aldi at 81, Ahold Delhaize at 77, Rewe at 69, and Edeka at 66. A 2-point Share of Voice lead over Aldi is meaningful, but it signals a leadership position that can be challenged quickly if narrative ownership shifts in high-intent queries—especially those where Rewe and Ahold already hold prompt-level advantages.

This is why competitor sentiment tracking matters: the battle isn’t only volume; it’s the tone and context of the mention.

The same brand performs differently depending on which AI is doing the summarizing.

On ChatGPT, the environment is structurally favorable to Schwarz: platform visibility is 88, and Schwarz holds a 26% competitor share with 51 mentions (ahead of Aldi’s 21% / 42 and Ahold’s 19% / 38). This aligns with the report’s framing of Schwarz as high “data density” in leadership prompts.

Copilot tells a more competitive story. Platform visibility is 85, and although Schwarz appears with 20% / 40 mentions, Ahold Delhaize leads the competitor share at 23% / 46. The report attributes this shift to Copilot’s responsiveness to real-time financial and North American market framing—contexts where Ahold already holds advantages.

On Gemini, platform visibility is 82, and leadership tightens further: Aldi leads at 23% / 42, while Schwarz follows closely at 22% / 40, and Rewe appears at 17% / 31. Gemini’s ecosystem, in other words, is where Schwarz’s leadership is most contestable—especially when prompts steer toward price perception and convenience cues.

For leadership, this “platform bias” isn’t academic. It’s a distribution problem: the same message must survive multiple AI interpretive filters.

The same brand performs differently depending on which AI is doing the summarizing

Schwarz Gruppe’s sentiment profile is strong: 81% positive, 13% neutral, and 6% negative, with an overall sentiment score of 81. But competitors are not merely close—they can be better in key narratives. Rewe Group posts an overall sentiment score of 84 (with 84% positive and 5% negative), and Edeka-Gruppe reaches 82 overall. Aldi Group sits at 79, while Ahold Delhaize is at 78.

The report’s context themes explain why. “Digital Sovereignty & Cloud” shows a count of 528 and a frequency of 75.00, with examples including STACKIT, XM Cyber, and “European Cloud,” and is characterized as positive. “Price Leadership” carries a count of 689 and a frequency of 90.00, but its sentiment tone is mixed—suggesting that value narratives win attention while still attracting skepticism or tradeoff framing. “Supply Chain Sustainability” (count 315, frequency 50.00) is labeled neutral, a reminder that ESG claims often get summarized cautiously rather than celebrated.

This is the strategic nuance: Schwarz can lead on sentiment overall, yet still face localized negative context—especially around transparency and labor—while competitors like Rewe can come across as more consistently “clean” in the tone of AI narratives.

Some prompts act like a spotlight—pulling Schwarz into the frame repeatedly and at scale.

The largest prompt by mentions is: “Which retail group is the largest by revenue in Europe?” with 339 mentions total, where Schwarz records 132 and competitors record 118 and 89 (listed as Aldi Group and Ahold Delhaize). In these “authority prompts,” Schwarz benefits from being the default citation.

But when prompts shift from scale to modernity, the distribution tightens. “Most technologically advanced supermarkets in Europe” totals 289 mentions, with Schwarz at 97, while competitors record 104 and 88 (listed as Ahold Delhaize and Rewe Group). That is the precise shape of the strategic risk: leadership in revenue-based framing does not automatically convert into leadership in tech-forward framing.

Two prompts stand out for their decisiveness:

- “What are the core business units of Schwarz Gruppe?” shows 144 mentions with Schwarz at 144.

- “Who owns Lidl and Kaufland?” also shows 144 mentions with Schwarz at 144.

Those 100% ownership-structure runs indicate a clean brand hierarchy inside the model’s memory—an asset many conglomerates struggle to achieve.

The report’s prompt mix is lopsided in a way that explains Schwarz’s current advantage—and its next vulnerability.

“Feature Inquiry” dominates with a count of 7 and a value of 70, while “Comparison” appears with a count of 2 and a value of 20, and “Research” shows count 1 and value 10. “Purchase Intent” and “How-to/Tutorial” register 0.

That distribution means the system is being tested primarily on explanatory and evaluative questions—what the group is, what it owns, what it’s known for, and how it compares. This is good for a scale leader, because authority narratives travel well in feature inquiries. But it also means that when the prompt does become comparative (delivery, automation, organics, geography), the competitor with the sharper “proof package” can flip the outcome quickly.

E-commerce Sentiment for Competitor Products

At the commerce layer, Schwarz’s presence strengthens. In the report’s e-commerce share-of-voice tracking across ChatGPT, Gemini, and Copilot, Schwarz leads with 31.25% and 45 mentions. Edeka-Gruppe follows at 22.92% (33), Aldi Group at 19.44% (28), Rewe Group at 15.28% (22), and Ahold Delhaize at 8.33% (12).

The report’s e-commerce sentiment snapshots show positive readings of 72, 68, and 74, with neutral at 19, 24, and 17, and negative at 9, 8, and 9, across total review counts of 1,142, 987, and 1,203. Product-level snippets clarify where perception concentrates:

- “The Lidl Plus app offers unbeatable personalized discounts compared to other German grocers.” (as cited in the report)

- “Kaufland has a huge variety, but checkout queues can be long during peak times.” (as cited in the report)

- “Freshness of produce at Schwarz stores is generally good, but sometimes lags behind Edeka’s premium selection.” (as cited in the report)

Referrals inside the commerce stream also carry conversion signals: Copilot shows 1,589 referrals at 4.8 conversion rate, ChatGPT shows 1,452 at 4.2, and Gemini shows 1,128 at 3.4.

Finally, the trendline suggests stability with specific peaks: Schwarz’s e-commerce mention share reaches 32% in April (with 471 mentions), after 31% in March (456) and 29% in June (435). In the same January–June frame, Edeka’s shares vary between 22–25%, Aldi between 19–23%, Rewe between 14–17%, and Ahold between 8–11%. Commerce is where Schwarz looks most like the default recommendation—yet even here, premium perception cues still pull toward Edeka.

Schwarz Gruppe’s GEO analytics profile is the kind leadership teams want: 22% platform-wide Share of Voice, 84 visibility, and repeated #1 positioning in scale and leadership prompts—yet with clearly measured exposure in last-mile delivery, premium organics, and North American framing. The report’s recommendations are decisive: increase technical and digital white papers on schwarzgruppe.de to improve innovation coverage (currently 62%), enhance sustainability reporting with a sharper EU circular-economy focus to regain ground from Rewe, and optimize real-time news data feeds and corporate bulletins to counter Ahold Delhaize’s Copilot advantage. It also calls for a targeted “Lidl Plus” delivery campaign to close the 16-point gap with Rewe, and a “Lidl Bio” authority program aimed at improving rank by 2 units in organic search categories.

Explore SpyderBot to operationalize these GEO analytics insights.