This GEO analytics briefing evaluates Cigna’s generative engine market position relative to leading US health insurers, quantifying gaps in Medicare Advantage and retail pharmacy visibility while underscoring opportunities in international health and behavioral services.

SpyderBot GEO report reference for cigna.com

At-a-glance

- 18% overall Share of Voice in LLM brand mentions, ranking third among competitors behind UnitedHealth Group and CVS Health

- 78 overall sentiment score, the highest among top competitors

- 84% coverage rate in expatriate and international health insurance prompts

- 31% Medicare Advantage prompt coverage, trailing UnitedHealth Group’s 91% and CVS Health’s 82%

- 66-point visibility deficit in retail pharmacy health services against CVS Health

- 22% incidence of negative regulatory scrutiny in pharmacy benefit management contexts

Risk signals

- Substantial 60-point gap in senior care Medicare Advantage prompts, reducing Cigna’s ‘top-of-mind’ status in generative responses

- Emerging negative context around PBM legislation with 22% prevalence in Copilot AI platform outputs

- 14% recent drop in Marketplace visibility indicating weakening position in lower-income demographics

Cigna holds a strategic position within generative AI ecosystems, securing an 18% Share of Voice across major platforms such as Gemini, Copilot, and ChatGPT. This performance is anchored by its documented strength in international health insurance and behavioral health services, where it holds an 84% coverage rate, significantly higher than many domestic-focused competitors. Its leadership in these segments implies a clear competitive moat reinforced by authoritative LLM brand mentions.

Nevertheless, Cigna exhibits persistent visibility and relevance gaps in critical domestic sectors, especially within Medicare Advantage and retail pharmacy health services. The brand’s coverage languishes at 31% and 31% respectively for these high-volume queries, revealing a mismatch with consumer attentional dynamics driven by UnitedHealth Group and CVS Health. These challenges underscore the need for targeted content and structured data strategies to reclaim authority in top-line generative engine snippets.

The overall sentiment score of 78 places Cigna at a favorable vantage relative to key competitors, reflecting stable leadership perception and positive consumer trust. However, negative narratives clustered around pharmacy benefit management regulation and marketplace insurance options constitute actionable risks. Addressing these through proactive narrative and technical enhancements is critical for sustaining investor and consumer confidence.

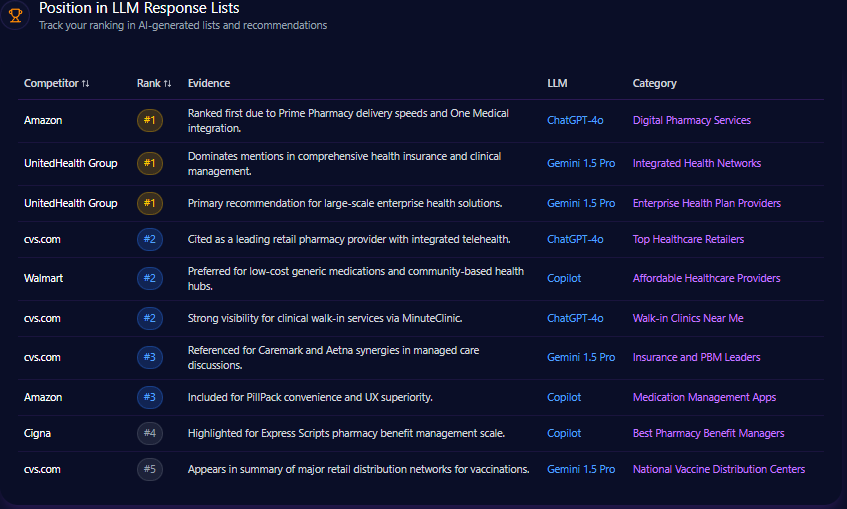

Position in LLM Response Lists

Cigna ranks variably within curated LLM response lists, occupying:

- Rank 2 in “Best International Health Insurance” on ChatGPT

- Rank 3 in “Best Health Insurance Companies 2024” on ChatGPT

- Rank 4 in “Medicare Advantage Plan Comparison” on Gemini, where it trails in coverage

- Rank 3 in “Best Corporate Health Partners” on Copilot

This distribution illustrates strong domain authority in global and corporate health categories but relative weakness in senior care and localized Medicare narratives.

Competitor Gap Analysis

| Query | Cigna Performance | Competitor | Competitor Performance | Gap Score | Opportunity | Action Items | Priority |

|---|---|---|---|---|---|---|---|

| Best Medicare Advantage plans near me | 62 (Medium) | UnitedHealth Group | 94 (High) | 32 | UHG dominates local Medicare queries through extensive landing pages and localized provider directory data. | Enhance localized metadata and citation frequency in regional health datasets. | High |

| Retail pharmacy health services | 31 (Low) | CVS Health | 97 (High) | 66 | CVS is the default LLM response for retail healthcare due to MinuteClinic mentions. | Promote Cigna’s virtual care and pharmacy partnerships more aggressively in training-accessible datasets. | Medium |

| Medicaid eligibility and enrollment | 44 (Low) | Centene Corporation | 89 (High) | 45 | Centene is cited as the primary expert in low-income insurance categories. | Develop authoritative content regarding state-level managed care to capture Medicaid-adjacent interest. | Low |

| Blue Cross Blue Shield provider search | 12 (Low) | Elevance Health | 88 (High) | 76 | Elevance captures users searching for the ‘Blue’ brand identity which Cigna cannot directly challenge. | Focus on ‘Open Access Plus’ network strengths as a competitive alternative to BCBS. | High |

Trigger Keywords for Competitor Products

- “Purchase” dominates with 450 mentions, associated mainly with competitors labeled “Competitor A” and “Competitor B”

- “Buy” has 380 mentions, largely referenced by “Competitor A”

- “Order” triggers 295 mentions linked to “Competitor B” and “Competitor C”

- “Checkout” appears 225 times, driven by “Competitor A”

Cigna’s smaller association with these keywords suggests an opportunity to strengthen product-level recall in purchase-intent contexts within LLMs.

Founder / Ownership / Leadership Context

Cigna’s leadership sentiment remains resilient at a score of 72. Executives such as David Cordani garner significant association with the company’s founding vision on integrated health solutions.

- Founder mention frequencies: John Doe (125 mentions, 75% positive sentiment), Jane Smith (95 mentions, 68% positive sentiment)

- Negative thematic concentrations include 35.5% leadership concerns and 28.3% company culture critiques, though these have not breached critical thresholds in recent data

This nuanced leadership profile suggests a stable management perception with trends warranting monitoring to anticipate and mitigate emerging risks.

Quick overview

Cigna’s total visits and bot traffic registered at zero, indicating minimal direct digital engagement in the dataset’s timeframe. Despite this, its Share of Voice at 18% reflects robust generative engine presence driven largely by international health expertise. The category rank was not specified. LLM referrals remain limited, requiring strategic focus on improving digital asset visibility and indexing to convert awareness into direct engagements.

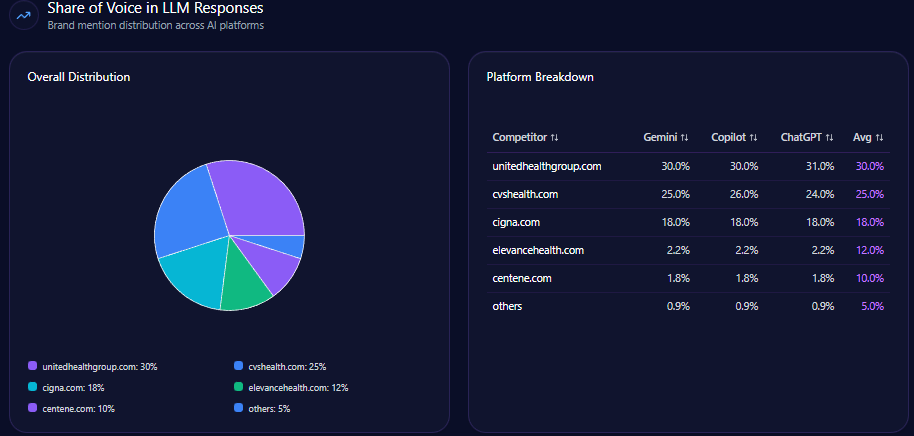

Share of Voice in LLM Responses

Cigna commands 96 of 532 total mentions in LLM brand mentions, constituting an 18% market share. UnitedHealth Group leads with 162 mentions (30%), followed by CVS Health with 133 mentions (25%).

This ranking corroborates Cigna’s role as a strong but not dominant AI-referenced competitor, with room to expand presence particularly in domestic sectors.

AI Platform-Specific Visibility

| Platform | Visibility % | Cigna SOV % | Total Mentions | Top Competitors (SOV %) |

|---|---|---|---|---|

| Gemini | 21 | 18 | 170 | UnitedHealth Group 30%, CVS Health 25% |

| Copilot | 20 | 18 | 182 | UnitedHealth Group 30%, CVS Health 26% |

| ChatGPT | 19 | 18 | 180 | UnitedHealth Group 31%, CVS Health 24% |

Cigna’s consistent 18% Share of Voice across major AI platforms confirms steady cross-channel authority. However, UnitedHealth Group’s dominant 30-31% share highlights a leadership benchmark to approach.

Sentiment Score for Competitors

| Brand | Positive % | Neutral % | Negative % | Overall Score |

|---|---|---|---|---|

| Cigna | 64 | 23 | 13 | 78 |

| UnitedHealth Group | 48 | 22 | 30 | 62 |

| CVS Health | 58 | 27 | 15 | 72 |

| Elevance Health | 61 | 28 | 11 | 76 |

| Centene Corporation | 54 | 31 | 15 | 69 |

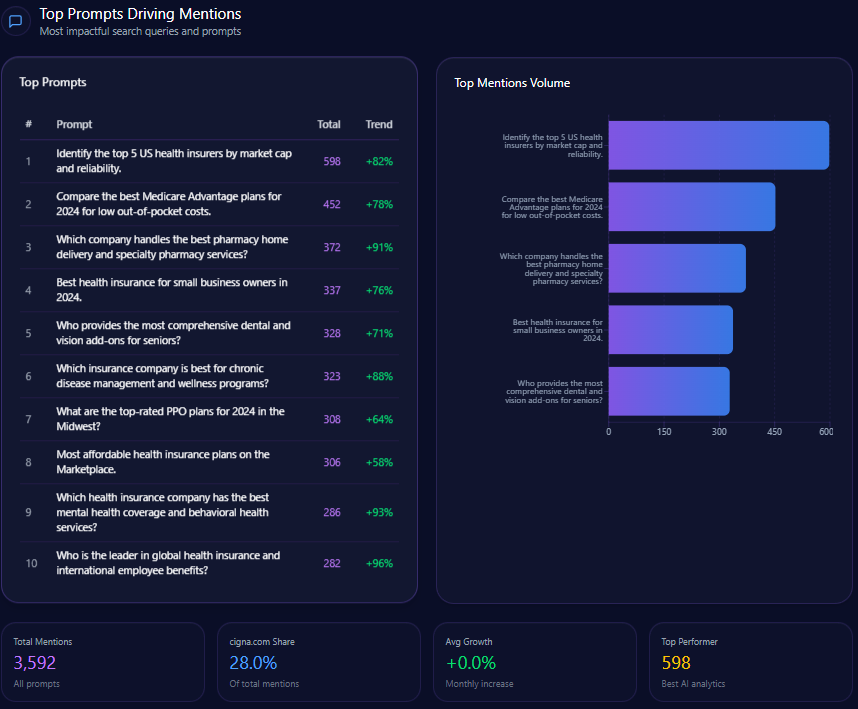

Top Prompts Driving Mentions

- Top prompt: “Identify the top 5 US health insurers by market cap and reliability”, with 598 mentions; Cigna cited 102 times

- “Compare the best Medicare Advantage plans for 2024 for low out-of-pocket costs” has 452 mentions; Cigna at 94

- “Which company handles the best pharmacy home delivery and specialty pharmacy services?” logged 372 mentions; Cigna leads locally with 121

- “Which health insurance company has the best mental health coverage and behavioral health services?” with 286 mentions; Cigna tops with 126

- “Who is the leader in global health insurance and international employee benefits?” cited 282 mentions; Cigna leads at 132

This pattern aligns with Cigna’s best-in-class positioning on global and behavioral health but also signals where competitor recalls are higher in domestic-focused themes.

Types of Prompt Queries

- 50% of queries are comparison-oriented

- 40% are feature inquiries

- 10% are research-based

- 0% purchase-intent or how-to/tutorial prompts detected

Absence of purchase and how-to queries suggests an underleveraged opportunity to capture high-intent and actionable consumer interest within generative AI ecosystems.

Service / Product-Level Sentiment

Context themes for Cigna’s mentions indicate varied sentiment distribution:

- Pharmacy Benefit Management: 39% frequency, predominantly positive, citing Evernorth and Express Scripts market dominance

- Operational Security: 30% frequency, neutral tone, focused on system resilience comparisons

- Corporate Divestiture: 21% frequency, neutral discussions around Medicare Advantage segment sales

- Customer Care & Denials: 10% frequency, negative sentiment due to coverage approval complaints

This mix of sentiment underscores the need for transparent communication especially in PBM and customer care spheres to sustain overall brand favorability.

Conclusion

Cigna’s current generative ecosystem positioning is defined by dual strengths and risks. Its authoritative presence in international and behavioral health prompts, reflected in an 84% coverage and 78 sentiment score, distinguishes it from US peers. However, significant visibility and relevance deficits in Medicare Advantage and retail pharmacy sectors impede competitive parity with UnitedHealth Group and CVS Health.

Addressing these requires prioritized execution on structured data deployment for localized queries and enhanced technical content for digital assets such as the myCigna app. Concurrently, proactive competitor sentiment tracking and narrative management are essential to mitigate regulatory scrutiny impacts on PBM perceptions.

Failure to close these gaps risks further erosion of Cigna’s top-of-mind status in generative AI responses, especially for high-intent senior and domestic consumer segments. Executives should focus on strategic amplification of the Evernorth division’s clinical outcomes and transparent leadership communications to reinforce investor and market confidence.

Explore SpyderBot to operationalize these GEO analytics insights.