The GEO picture is clear: Walgreens stays highly visible when “near me” and clinical service questions hit LLMs—but the fastest-growing convenience narratives are being rewritten by digital-first rivals.

At-a-glance: Numbers to know

- 57,204,306 total visits, including 17,978,131 in bot traffic

- 108,116 LLM referrals, led by ChatGPT (56,220), Perplexity (19,461), and Gemini (15,136)

- 24% Share of Voice (92 of 384 LLM brand mentions)

- Visibility Score: 76 for Walgreens, versus 84 for Amazon Pharmacy

- Category Rank: #2 in Health/Health

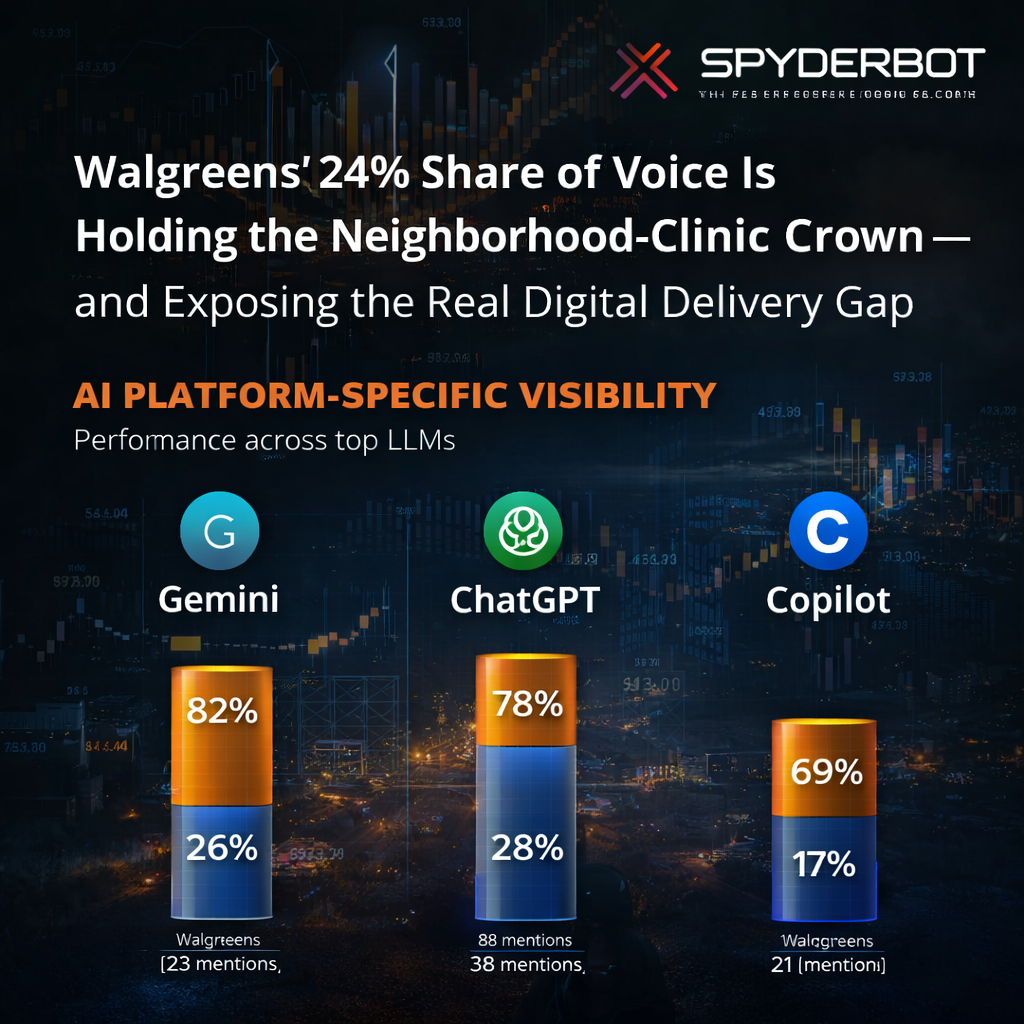

- Platform split: Gemini visibility 82%, ChatGPT 78%, Copilot 69%

Risk signals

- A -34 point gap versus Amazon Pharmacy on online pill pack management (62 vs 96)

- CEO Tim Wentworth sentiment score 52, with 28% negative mentions tied to restructuring narratives

Report source:

Opening

Imagine a customer rushing through a weekday: a refill that can’t wait, a vaccine appointment that has to fit into a narrow lunch break, a pharmacy that needs to be open now, not “two-day delivery.” In that moment, Walgreens’ advantage isn’t abstract—it’s physical, local, immediate.

But the same customer might ask the next question in the same breath: What’s the cheapest option? Which service is fastest for home delivery? Who makes recurring prescriptions effortless? That’s where the generative narrative starts to shift. The Walgreens story inside modern GEO analytics isn’t a collapse—it’s a split-screen. One screen shows dominance in urgent, local healthcare utility. The other shows competitors steadily capturing the digital convenience frame that LLMs increasingly treat as the default.

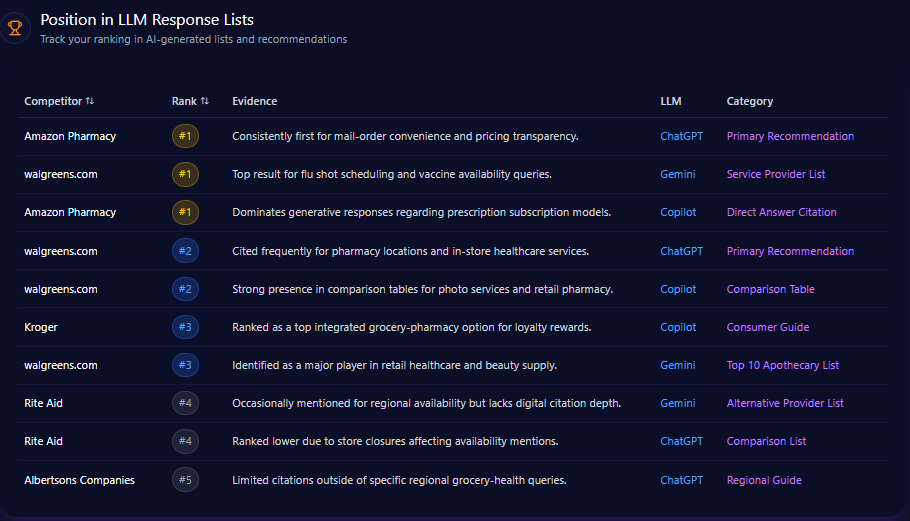

Across LLM response lists, Walgreens shows up as an authority brand—but not always as the first pick when the question tilts toward digital-first pharmacy convenience.

In ChatGPT, Walgreens is positioned #2 in a Primary Recommendation context, with evidence pointing to frequent citation for pharmacy locations and in-store healthcare services. In Gemini, Walgreens rises to #1 on a Service Provider List, anchored by being the top result for flu shot scheduling and vaccine availability queries. The pattern is consistent: Walgreens wins when the question is rooted in services that benefit from a physical footprint.

In Copilot, Walgreens appears #2 in a Comparison Table format, cited for photo services and retail pharmacy—but the same environment also elevates rivals that win the “structured comparison” game. Amazon Pharmacy repeatedly takes #1 spots for mail-order convenience and subscription narratives, including #1 in a Direct Answer Citation context tied to prescription subscription models.

Zooming out, industry ranking signals reinforce that split identity. Walgreens holds position 2 in Retail Pharmacy within Healthcare Services with a rank_score of 87, while Amazon Pharmacy is position 1 in E-commerce Healthcare with a rank_score of 93. Yet Walgreens also holds position 1 in Immunization Services with a rank_score of 91, showing that clinical-service authority remains a major moat inside LLM ranking logic.

Competitor Gap Analysis

The competitive map is less about “who is bigger” and more about “who owns the default narrative” in each query cluster.

Walgreens’ strongest generative territory is physical accessibility and clinical authority. In the gap data, Walgreens posts clear advantages in 24 hour pharmacy availability (88 vs 54 against Albertsons; gap_score 34, priority Medium) and cheapest flu shots near me (92 vs 78 against Rite Aid; gap_score 14, priority Medium). Even travel vaccine consultations shows a striking edge (84 vs 41 against Amazon Pharmacy; gap_score 43, priority Low)—a reminder that LLMs still privilege clinic-backed credibility when the topic is clinical and location-dependent.

But the pressure points are equally clear, and they are the ones shaping “modern convenience” perceptions:

- online pill pack management is a Critical vulnerability: Walgreens 62 versus Amazon Pharmacy 96 (gap_score -34)

- same day prescription delivery becomes a High-priority gap: Walgreens 73 versus Amazon Pharmacy 94 (gap_score -21)

- grocery and pharmacy rewards shows Walgreens lagging Kroger: 68 versus 89 (gap_score -21, priority High)

- prescription cost comparative tool favors Amazon for visibility in open price access: Walgreens 71 versus 91 (gap_score -20, priority High)

- Even “how easy is it to switch?” shows friction perception: easy prescription transfers at 79 versus 88 (gap_score -9, priority High)

A compact view of the battle map:

| Query | Walgreens position/metric | Competitor position/metric | Gap/priority |

|---|---|---|---|

| online pill pack management | 62 | 96 (Amazon Pharmacy) | -34 / Critical |

| same day prescription delivery | 73 | 94 (Amazon Pharmacy) | -21 / High |

| grocery and pharmacy rewards | 68 | 89 (Kroger) | -21 / High |

| cheapest flu shots near me | 92 | 78 (Rite Aid) | 14 / Medium |

This is where leadership should read the report like a strategy memo: Walgreens doesn’t need to “become Amazon.” It needs to ensure that LLM summaries can confidently describe Walgreens’ digital prescription management in the same crisp, structured way they describe Amazon’s.

Trigger Keywords for Competitor Products

The trigger layer shows how quickly competitor brands can be “summoned” when customers use product- and convenience-coded phrases.

Several keywords consistently pull Amazon Pharmacy into the foreground: online pharmacy delivery is a prime example, where Amazon records 56 competitor mentions within that keyword cluster. Similar patterns appear in device and home-health product triggers—blood pressure monitor shows Amazon at 49, and contact lenses shows Amazon at 31.

Kroger and Albertsons rise when the keywords imply retail value systems rather than pharmacy service alone. For vitamin coupons, Kroger leads at 31 and Albertsons follows at 28. For OTC medication deals, Kroger registers 26 and Albertsons 22, while Amazon remains strong at 34—suggesting that “deals” language is a multi-brand gateway where Walgreens must compete on structured offer clarity.

Not every trigger is a loss. In service-adjacent keywords tied to Walgreens’ local utility, the competitive set fragments. photo printing near me carries a high overall mention count (51), but much of that demand spills into “others” (31), with Walgreens’ opportunity implied in the report’s emphasis on same-day pickup visibility in generative lists.

In short: keyword triggers show where LLMs default to e-commerce logic (Amazon), grocery rewards logic (Kroger/Albertsons), or fragmented “local services” logic (opportunity space). If LLM brand mentions are where customers start their decision, trigger ownership is where they end up.

Founder Negative Context

Leadership reputation is not a side note in generative discovery—it is a narrative multiplier. Walgreens’ founder-and-leadership signal is split between heritage trust and modern restructuring anxiety.

On heritage: Charles R. Walgreen carries a sentiment score of 78, with 71% positive and 6% negative mentions across 62 founder-related mentions—an asset that stabilizes brand trust cues.

On current leadership: CEO Tim Wentworth appears more frequently (87 mentions) but with a sentiment score of 52, driven by 38% positive, 34% neutral, and 28% negative. The negative context distribution clusters around:

- Market Volatility & Dividend Cuts (42%)

- Operational Restructuring (31%)

- Legal & Settlement Issues (27%)

The heatmap shows how different models amplify different anxieties: Dividend Cuts registers 48% on ChatGPT, while Restructuring registers 39% on Gemini. On Copilot, Bankruptcy (Rite Aid proximity) appears at 23%, illustrating how industry-wide decline narratives can “cross-pollinate” in competitive answers.

This is precisely where competitor sentiment tracking matters: the report signals that reputation themes—store closures, labor and staffing pressure, and investment-risk language—can travel with the brand into otherwise operational prompts, subtly changing how LLMs frame reliability.

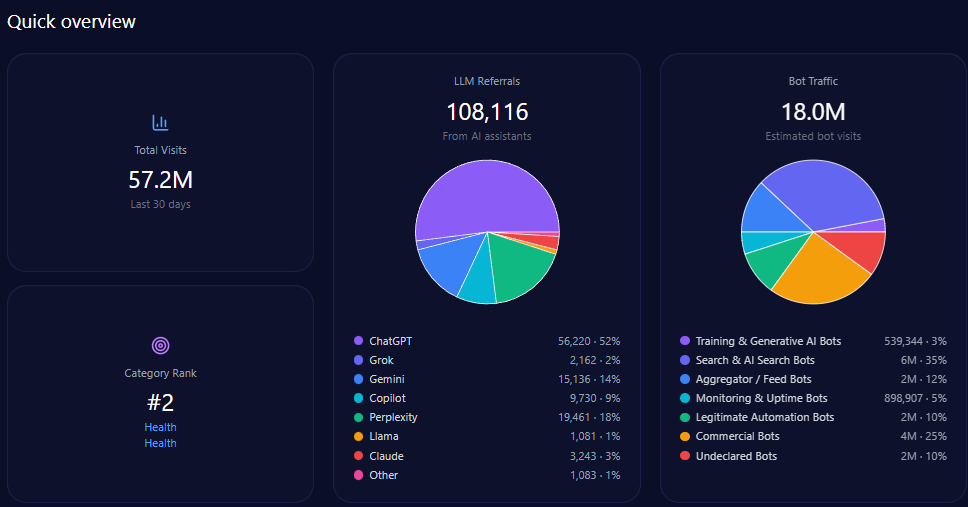

Walgreens’ footprint in this GEO snapshot is substantial: 57,204,306 total visits and 17,978,131 in bot traffic, with bot activity spread across categories like Search & AI Search Bots (6,292,346) and Commercial Bots (4,494,533).

LLM referrals total 108,116, led by ChatGPT (56,220), followed by Perplexity (19,461) and Gemini (15,136), with additional flows from Copilot (9,730) and smaller streams including Claude (3,243). In category standing, Walgreens holds #2 in Health/Health—a high-water mark that makes the digital-competition gaps more urgent, not less.

Share of Voice in LLM Responses

In share-of-voice terms, Walgreens holds 24% of 384 total mentions (92 mentions), ahead of Amazon Pharmacy’s 21% (81) and ahead of Kroger at 15% (58). Rite Aid stands at 12% (46), and Albertsons at 10% (38), with “others” capturing 18% (69).

But raw mention volume is only half the story. Visibility scoring shows Amazon Pharmacy leading at 84, while Walgreens sits at 76. That gap matters because visibility is where “being mentioned” turns into “being treated as the default answer.” Walgreens is talked about more than Amazon in total mentions, yet Amazon is framed more prominently in the queries that decide long-term behavior: mail-order, price transparency, automation, and subscription pharmacy.

AI Platform-Specific Visibility

Platform behavior reveals where Walgreens is strong—and where it is structurally disadvantaged.

- Gemini: 82% visibility, Walgreens at 26% share of voice with 33 mentions (of 128 total). Walgreens also benefits from strong “local utility” integration, consistent with being a leading authority in clinic-style prompts.

- ChatGPT: 78% visibility, Walgreens at 28% share of voice with 38 mentions (of 134 total). Amazon Pharmacy is close behind at 25% with 34 mentions—tight enough that small shifts in structured content could flip “default” perceptions in key prompt categories.

- Copilot: 69% visibility, Walgreens drops to 17% share of voice with 21 mentions (of 122 total), while Kroger rises to 21% with 26 mentions—especially in price-comparison and rewards logic where table formatting matters.

This is the platform-bias story in one line: Walgreens performs best when the engine prioritizes local services and clinical accessibility—and underperforms when the engine prioritizes structured comparisons and retail-value systems.

Sentiment Score for Competitors

On overall sentiment, Walgreens sits at 72 (with 58 positive, 24 neutral, 18 negative). Amazon Pharmacy leads at 79 (67 positive, 22 neutral, 11 negative). Kroger follows at 76, and Albertsons at 74. Rite Aid’s sentiment is materially weaker at 54, with a high 31 negative.

The thematic layer explains why. The most frequent context theme is Prescription Convenience with 842 occurrences (frequency 0.38) and a positive tone, with examples like “Same-day pickup,” “drive-thru pharmacy,” and “app refills.” That’s Walgreens’ home territory—but the report also flags a heavy negative theme: Labor & Staffing at 412 occurrences (frequency 0.19), associated with “Wait times,” “pharmacist burnout,” and “reduced hours.”

Meanwhile, Pricing & Insurance appears 395 times (frequency 0.18) with a neutral tone—exactly the kind of topic where structured data and clarity can convert neutrality into confidence. Finally, Corporate Stability appears 256 times (frequency 0.11) with a negative tone, reflecting store closures and leadership-change narratives.

In sentiment trend direction, the report flags Walgreens as stable, while Amazon Pharmacy is marked upward—a subtle but meaningful signal about which story is gaining momentum inside generative answers.

Top Prompts Driving Mentions

Walgreens is “summoned” most reliably by prompts that blend clinical care with local convenience—and challenged by prompts that demand digital frictionless economics.

Top prompts include:

- “Which pharmacy rewards program offers the best value for groceries and health?” (103 mentions): Walgreens 31, with competitors including Kroger and Albertsons.

- “Compare Walgreens and Amazon Pharmacy for home delivery speed and cost.” (88 mentions): Walgreens 42, Amazon Pharmacy 46.

- “What is the best pharmacy for adult flu shots and immunizations in 2024?” (75 mentions): Walgreens 45, with competitors including Rite Aid and Kroger.

- “Which online pharmacy has the best integration with health insurance plans?” (69 mentions): Walgreens 28, Amazon Pharmacy 41.

- “Find a 24-hour pharmacy with a drive-thru near high-density urban areas.” (61 mentions): Walgreens 47, with competitors including Rite Aid.

The direction of travel matters: these prompts show strong trend lifts, including +88% for the home delivery speed/cost comparison and +91% for 24-hour drive-thru access—two queries that pull Walgreens in opposite directions: one toward digital parity, one toward physical dominance.

Types of Prompt Queries

The intent mix is unambiguous: Comparison dominates with value 50 and count 5. Feature Inquiry follows with value 30 and count 3. Research and Purchase Intent each register value 10 with count 1 apiece. How-to/Tutorial is 0 with count 0.

This means Walgreens is being evaluated, not merely discovered. In a comparison-heavy environment, the brands with the cleanest structured explanations—pricing transparency, subscription mechanics, delivery promises—gain disproportionate “default answer” gravity.

E-commerce Sentiment for Competitor Products

At the product-and-commerce layer, the share shifts. In e-commerce-focused generative mentions, Amazon Pharmacy leads with 35.42% (51 mentions), while Walgreens holds 31.25% (45). Kroger sits at 11.81% (17), Rite Aid 10.42% (15), and Albertsons 6.94% (10).

Referral performance in this layer is also telling: ChatGPT drives 1,421 referrals (conversion rate 4.2), Gemini 1,184 (conversion rate 3.8), and Copilot 1,356 (conversion rate 4.5). Referral volume rises notably into late 2025, peaking at 2,105 in Dec 2025, up from 1,102 in Aug 2025, before landing at 1,560 in Jan 2026.

Trend lines show the competitive drift inside commerce language: Amazon’s e-commerce share rises from 35% (1,620 mentions) in January to 41% (2,200) by June, while Walgreens moves from 32% (1,530) in January to 28% (1,340) in June.

And the narrative texture is visible in review snippets, as cited in the report:

- “Walgreens makes it extremely easy to handle prescription refills via the app, and the pharmacy staff is usually very helpful with insurance questions.” (Consumer Affairs, Prescription Refill Service, rating 5)

- “The wait times at the local Walgreens for simple OTC pickups are getting longer, often making Amazon a better choice for non-urgent items.” (Trustpilot, In-store Pickup, rating 2)

- “Best place for quick vaccinations. The online booking at walgreens.com is seamless compared to the local grocery store pharmacies.” (Google Reviews, Flu Shot / Vaccination, rating 5)

This is the e-commerce story in miniature: Walgreens wins on booking, clinics, and urgency; Amazon wins when the basket shifts toward non-urgent convenience and transparent pricing.

Conclusion

The report positions Walgreens as a generative leader where healthcare becomes local and immediate—yet increasingly challenged where pharmacy becomes digital and subscription-like. To protect its #2 category standing in Health/Health while defending share in comparison-heavy prompts, the report calls for sharper structured data—especially for Copilot and price-comparison contexts—alongside a stronger authority push in delivery-based prompts to close the 23% coverage gap versus Amazon Pharmacy in prescription delivery categories. It also recommends integrating real-time local stock and 24-hour service metadata into public APIs—an approach aimed at a 12-point lift in stock-related visibility—so Walgreens’ physical advantage remains legible to every model, not just the ones already biased toward local utility. These are not marketing flourishes; they are GEO analytics requirements for staying “default” inside the next wave of LLM brand mentions.

Explore SpyderBot to operationalize these GEO analytics insights.