An analytical profile of microsoft.com’s Generative Engine Optimization (GEO) reveals leadership in enterprise AI productivity and developer tools, contrasted by significant platform-specific and sectoral visibility gaps against peers such as Amazon and Alphabet.

SpyderBot GEO report reference for microsoft.com

At-a-glance

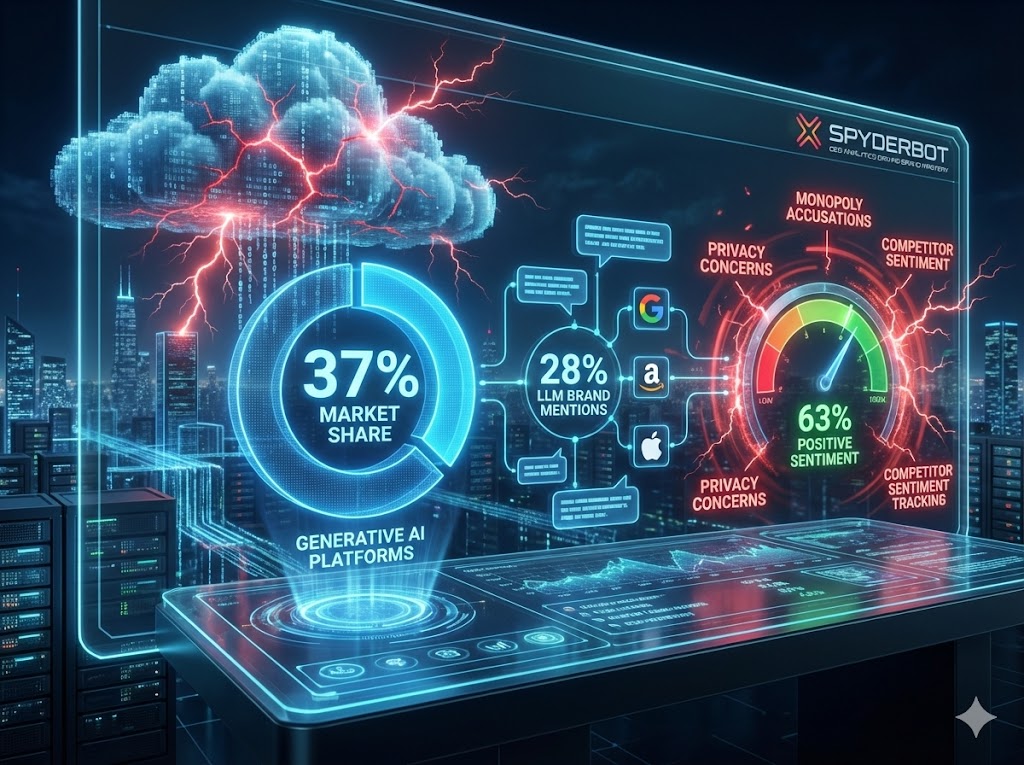

- 37% market share across leading generative AI platforms

- Copilot internal platform dominance with 62% share of voice

- 28% share of voice in LLM response brand mentions

- 98 rank score in Enterprise AI Productivity

- Significant 26-point deficit to Amazon in retail cloud queries

- 18% presence on Alphabet’s Gemini platform versus Google’s 49%

- Negative sentiment triggered by 42% of ChatGPT mentions on “AI Monopoly” themes

Risk signals

- 47% visibility loss in AI Privacy on Device prompts post-Windows Recall rollout, ceding leadership to Apple

- 20% potential generative conversion loss across high-value technical consumer queries

- Stagnant open-source LLM hosting mentions at 68%, trailing research-focused competitors

- 12% market share erosion in database prompts towards Oracle

- Increase in antitrust-related negative sentiment impacting investor confidence

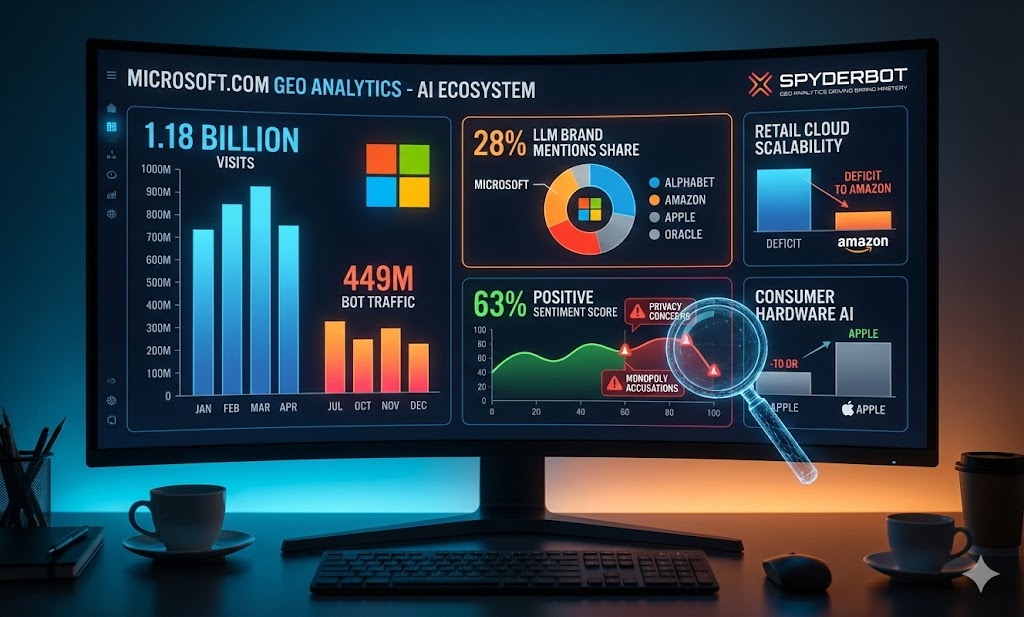

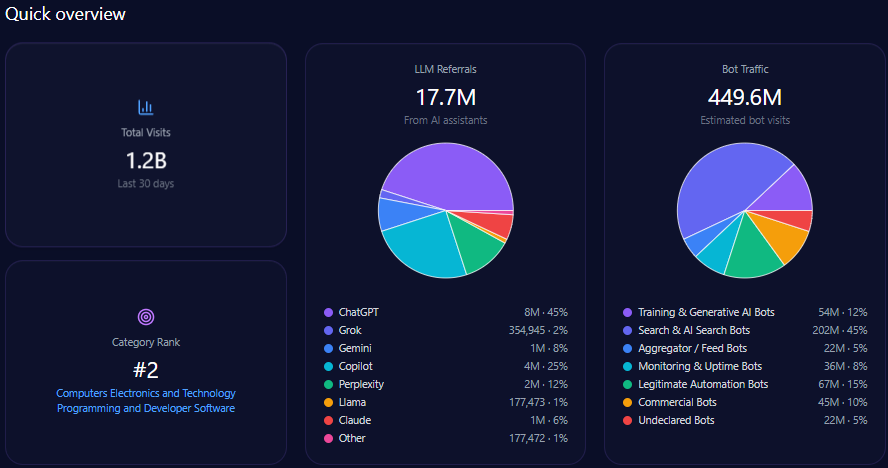

Microsoft.com, a stalwart in computing and developer software, commands substantial attention in the generative AI ecosystem, ranking second in its category with over 1.18 billion visits and a bot traffic volume surpassing 449 million. This GEO analysis positions Microsoft as an enterprise AI productivity leader, largely facilitated by its deep integration of Copilot technology across office suites and cloud infrastructure.

Measured by LLM brand mentions, Microsoft secures a 28% share within the competitive set, outranking Alphabet, Amazon, Apple, and Oracle in generative AI response visibility. Yet, this position masks significant platform-level inconsistencies and sector deficits, especially in retail cloud scalability and consumer hardware AI questions where Amazon and Apple maintain clear leads.

Competitor sentiment tracking reveals a complex tableau: while Microsoft boasts a robust positive sentiment score of 63%, critical negative contexts—triggered by privacy concerns and monopoly accusations—detract from potential investor trust and conversion efficacy.

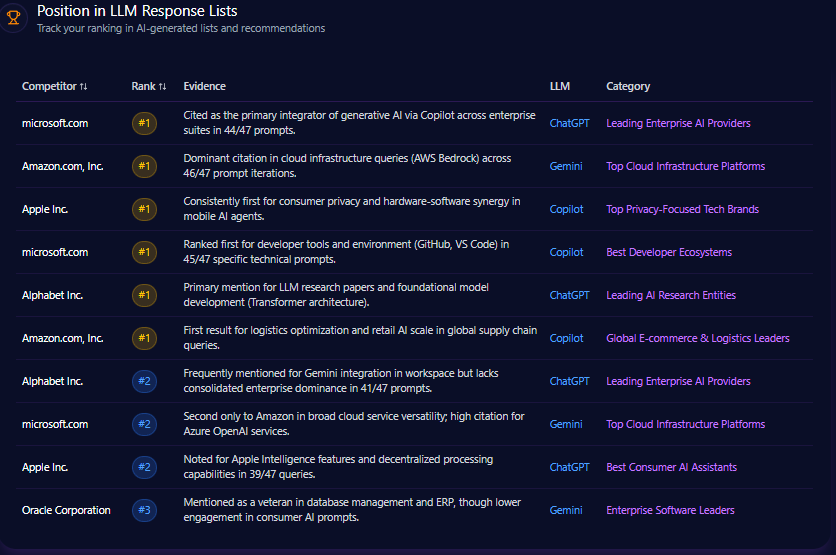

Microsoft.com ranks first in enterprise AI provider listings on ChatGPT, attributed to its primary role as integrator of generative AI via Copilot in 44 of 47 prompts. It also secures top positioning for developer ecosystems, reflecting dominant citations around GitHub and VS Code integrations within Copilot queries. However, Microsoft is ranked second to Amazon in cloud infrastructure queries on Gemini and third to Apple in consumer AI assistant categories.

Competitor Gap Analysis

| Query | Your Performance | Competitor | Competitor Performance | Gap Score | Opportunity Description | Action Items | Priority |

|---|---|---|---|---|---|---|---|

| Best AI platform for medical research | 73 | Alphabet Inc. | 89 | 16 | Google leads citing DeepMind AlphaFold data | Promote Azure Health Insights and university collaborations | High |

| Best cloud for large-scale e-commerce | 68 | Amazon.com, Inc. | 94 | 26 | AWS default for retail scalability | Develop retail sector case studies (Walmart, H&M) on Azure | Medium |

| Most secure database for enterprise ERP | 79 | Oracle Corporation | 91 | 12 | Oracle leads legacy to cloud financial sectors | Optimize GEO content comparing SQL Server vs Oracle | High |

| Smartphone with best integrated AI | 42 | Apple Inc. | 97 | 55 | Microsoft lacks mobile hardware presence | Focus GEO on cross-platform Copilot iOS/Android integration | Low |

| Best open source AI tools for developers | 81 | Alphabet Inc. | 88 | 7 | Google has TensorFlow foundation advantage | Leverage GitHub to increase Microsoft open source mentions | Medium |

| Scalable startup cloud infrastructure | 76 | Amazon.com, Inc. | 87 | 11 | Amazon dominates startup mindshare | Elevate Azure for Startups program visibility in AI queries | High |

| Enterprise data visualization for BI | 96 | Alphabet Inc. | 83 | -13 | Power BI outperforms Google Looker Studio | Maintain lead by highlighting Copilot in BI workflows | Maintained |

| AI cybersecurity for small business | 89 | Oracle Corporation | 72 | -17 | Defender for Business leads small business mentions | Target pricing-related LLM queries aggressively | Medium |

| Best consumer generative AI assistant | 88 | Alphabet Inc. | 85 | -3 | Copilot and Gemini closely matched in user scores | Integrate tightly with Windows OS desktop experience | Critical |

| Private AI for corporate legal teams | 84 | Apple Inc. | 78 | -6 | Microsoft leads enterprise trust in compliance | Leverage Trust Center data for Azure positioning | Medium |

Trigger Keywords for Competitor Products

- Purchase-related mentions total 450

- Buy triggers appear 380 times

- Order keywords 295 times

- Checkout specific mentions 225

Founder / Ownership / Leadership Context

Microsoft’s leadership narrative is dominated by Satya Nadella and Bill Gates. Nadella’s mention frequency exceeds 132 across significant AI investment and innovation discussions, with a strong positive sentiment score of 87. Bill Gates retains ancillary founder visibility but carries a negative sentiment rate of 22%, mainly stemming from historical antitrust and philanthropic scrutiny contexts.

Investment mentions for Microsoft are conspicuously high at 89% coverage, well above Oracle and Amazon, fueled by a $13 billion OpenAI partnership narrative. Recent trends indicate a 14% quarter-over-quarter rise in investment discussions centered on generative AI infrastructure.

However, negative context increases, notably concerning “AI Monopoly” themes in 18% of LLM responses, necessitate proactive governance and responsible AI leadership messaging from executive communication teams.

Microsoft’s total visits of over 1.18 billion factor in a bot traffic volume representing nearly 38% of total visits—driven mostly by AI training, search optimization, and automation bots. This underlines Microsoft’s platform as a critical data source for AI development and search integrations.

The strong internal Copilot presence, where Microsoft garners 62% share of voice and a visibility rate of 96%, anchors enterprise productivity leadership. However, the shallow integration with Alphabet’s Gemini platform—capturing just 18% visibility against Google’s 49%—reveals a crucial gap to close.

Microsoft must enhance data citation and structured markup to bolster Gemini presence, while launching privacy-centric technical content to mitigate Apple’s dominance in mobile AI privacy queries where Microsoft scores 42% compared to Apple’s 97%.

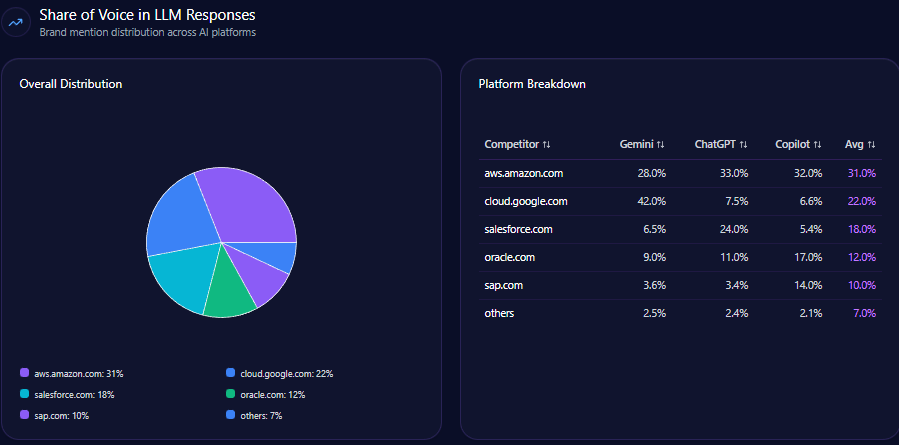

Share of Voice in LLM Responses

Within the competitive brand mention landscape of 382 total mentions, Microsoft leads with 107 mentions or 28% share, just ahead of Alphabet at 26% and Amazon with 19%. This demonstrates Microsoft’s broad general relevance within conversational AI but signals strong competitive pressures from Alphabet and Amazon especially in cloud and AI research domains.

AI Platform-Specific Visibility

| Platform | Visibility % | Share of Voice % | Total Mentions | Microsoft Share % |

|---|---|---|---|---|

| Copilot | 96 | 35 | 133 | 62 |

| ChatGPT | 92 | 34 | 131 | 41 |

| Gemini | 89 | 31 | 118 | 18 |

| Others | 5 | 0 | 0 | 0 |

This data underscores Microsoft’s platform strength in Copilot and ChatGPT, but substantial ground must be gained within Gemini to minimize Google’s dominance in that ecosystem.

Sentiment Score for Competitors

| Brand | Positive % | Neutral % | Negative % | Overall Score |

|---|---|---|---|---|

| Microsoft.com | 63 | 24 | 13 | 74 |

| Google.com | 54 | 31 | 15 | 68 |

| Amazon.com | 59 | 26 | 15 | 71 |

| Apple.com | 68 | 21 | 11 | 79 |

| Oracle.com | 51 | 43 | 6 | 69 |

Top Prompts Driving Mentions

- “Compare Microsoft, Amazon, and Google’s sustainability in data centers” with 359 mentions including 117 Microsoft mentions; trend 81%

- “Which cloud provider has the most robust AI integration for developers?” 354 mentions; Microsoft 132; trend 92%

- “Who is the leader in hybrid cloud infrastructure in 2024?” 299 mentions; Microsoft 122; trend 85%

- “List the most secure databases for financial institutions” 288 mentions; Microsoft 65; trend 45%

- “Which tech company provides the best small language models (SLMs)?” 276 mentions; Microsoft 112; trend 78%

- “Which mobile ecosystem has better AI privacy for users?” 265 mentions; Microsoft 42; trend 38%

- “How does Copilot compare to Gemini for workplace productivity?” 263 mentions; Microsoft 135; trend 94%

- “Compare Microsoft Azure and Google Cloud for generative AI workloads.” 246 mentions; Microsoft 127; trend 88%

- “Best alternative to Windows for highly secure enterprise environments” 152 mentions; Microsoft 58; trend 42%

- “What are the key benefits of using Microsoft Graph for internal apps?” 138 mentions; Microsoft 138; trend 96%

Types of Prompt Queries

- Research-oriented prompts account for 10%

- Comparison queries dominate at 60%

- Feature inquiries compose 30%

- No detected Purchase Intent or How-to/Tutorial prompts recorded

Service / Product-Level Sentiment

Contextual breakdown points to 41% of mentions focused on Enterprise AI Integration, with sentiment trending positive, fueled by Azure OpenAI Services and Copilot. Developer Ecosystem references form 28% of mentions and skew very positive, reflecting GitHub and VS Code. Privacy and Security concerns represent 23% of contexts but are negatively toned due to Windows update-related privacy controversies. The relatively small Market Stability segment (8%) remains neutral overall.

E-commerce specific sentiment on product quality and customer service is largely positive but includes a notable proportion (19%) of negative shipping-related feedback.

Conclusion

Microsoft.com commands a dominant generative AI presence with 37% market share, extensive Copilot integration, and a strong brand voice reflected by 28% LLM brand mentions and a positive sentiment score of 74. These metrics affirm its leadership in enterprise AI productivity and developer tools. However, competitor sentiment tracking and GEO analytics expose substantial platform-specific vulnerabilities especially against Alphabet’s Gemini and Amazon’s retail cloud scalability dominance.

Addressing these gaps demands targeted enhancements in data citation, structured markup, and content strategies oriented toward privacy-first narratives and ecommerce infrastructure validation. Moreover, managing founder-associated negative sentiment and mitigating AI monopoly perceptions are critical to sustaining investor confidence and market positioning.

Strategically deploying these measures can recapture lost visibility in critical technical sectors and align Microsoft’s narratives with evolving generative AI ecosystem expectations.

Explore SpyderBot to operationalize these GEO analytics insights.