An analytic GEO analytics briefing on Oracle’s generative AI ecosystem performance, competitive visibility, and LLM brand mentions across top AI platforms.

SpyderBot GEO report reference for oracle.com

At-a-glance

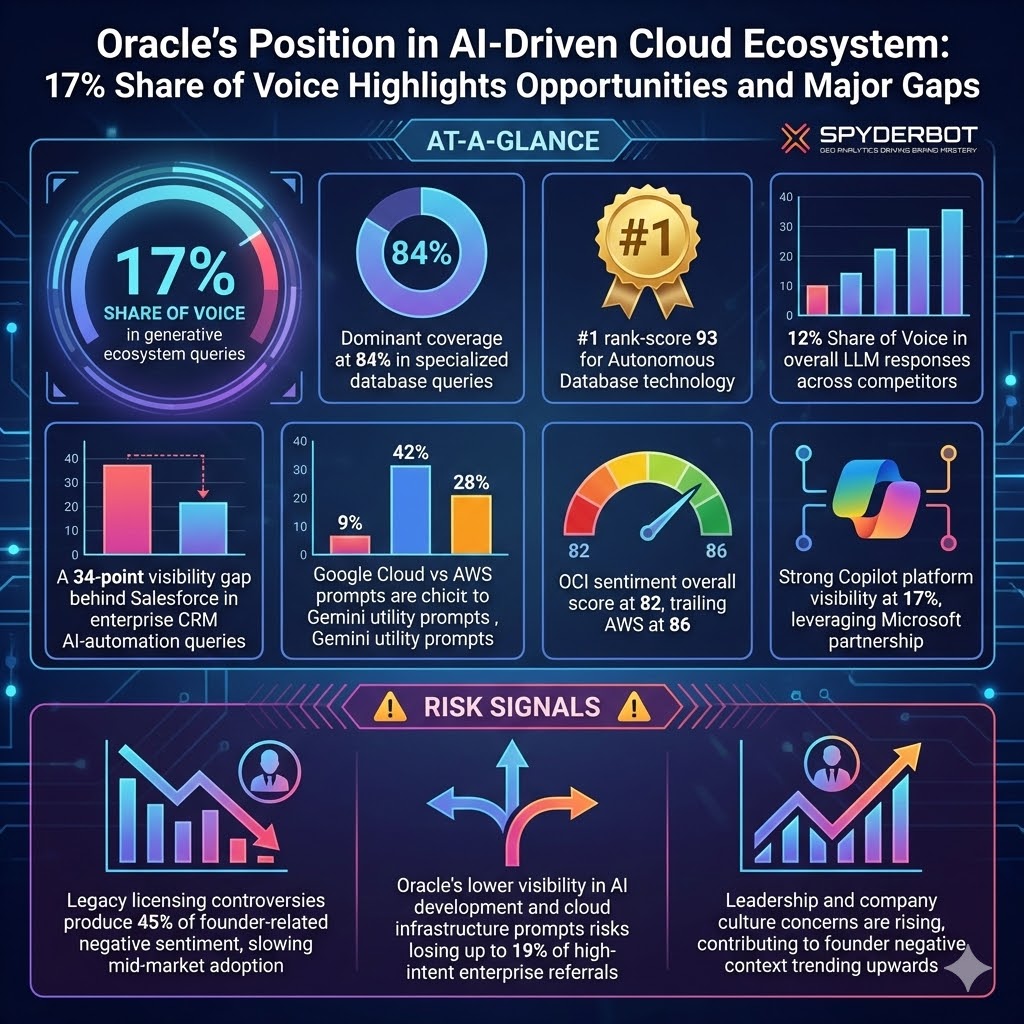

- 17% Share of Voice in generative ecosystem queries.

- Dominant coverage at 84% in specialized database queries.

- #1 rank-score 93 for Autonomous Database technology.

- 12% Share of Voice in overall LLM responses across competitors.

- A 34-point visibility gap behind Salesforce in enterprise CRM AI-automation queries.

- 9% Share of Voice on Gemini cloud utility prompts, trailing Google Cloud’s 42% and AWS’s 28%.

- OCI sentiment overall score at 82, trailing AWS at 86.

- Strong Copilot platform visibility at 17%, leveraging Microsoft partnership.

Risk signals

- Legacy licensing controversies produce 45% of founder-related negative sentiment, slowing mid-market adoption.

- Oracle’s lower visibility in AI development and cloud infrastructure prompts risks losing up to 19% of high-intent enterprise referrals.

- Leadership and company culture concerns are rising, contributing to founder negative context trending upwards.

Opening

Oracle retains a resilient foothold within the evolving generative AI and cloud infrastructure landscape, securing a 17% Share of Voice across key ecosystem queries. This share illustrates substantive brand recall in AI training performance and specialized database services, notably with its Autonomous Database holding a rank-score of 93. Despite these strengths, Oracle’s general cloud utility mentions lag considerably behind dominant competitors such as AWS and Google Cloud, suggesting targeted strategic communication gaps.

The brand’s current visibility skew favors well-defined technical niches—such as database scalability and AI training performance—where Oracle commands plus capacity in Artificial Intelligence infrastructure, evidenced by an OCI sentiment score of 82 fueled by partnerships with NVIDIA and Microsoft. However, Salesforce’s near monopolization of AI-automation CRM queries and Google Cloud’s dominance in AI platform references highlight significant opportunity areas.

To capitalize on its existing strengths, Oracle must address visible gaps in brand prompt coverage and founder-related legacy controversies, using data-driven content strategies to improve competitor sentiment tracking and reduce the friction caused by complex licensing narratives prevalent in LLM brand mentions.

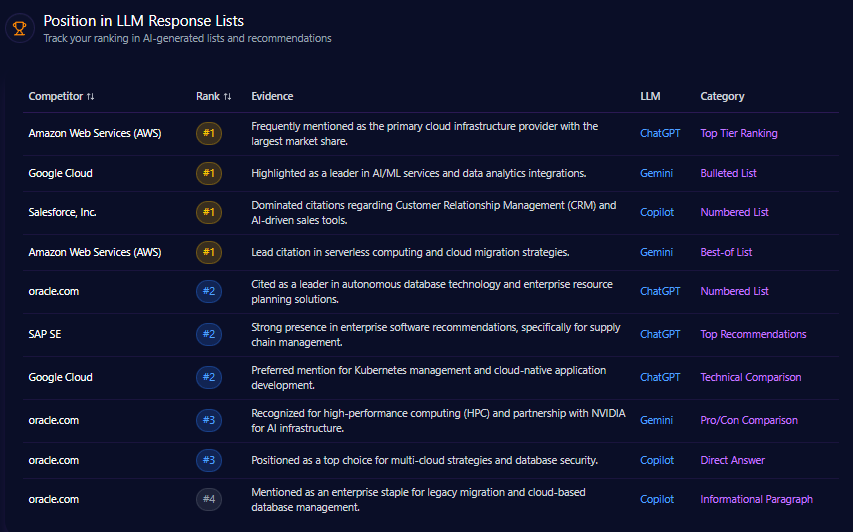

Position in LLM Response Lists

Oracle consistently appears within top-tier generative AI lists but generally ranks below competitors in prominence. For instance, it holds a second rank in ChatGPT’s numbered lists for autonomous databases and ERP solutions, yet never claims the primary position held by AWS or Google Cloud in infrastructure and AI services.

This intermediate rank illustrates Oracle’s recognized expertise while underscoring its struggle to secure sector leadership in broader cloud infrastructure or CRM AI categories, where competitors rank first per LLM response evidence.

Competitor Gap Analysis

| Query | Oracle Score | Competitor | Competitor Score | Gap | Opportunity | Action | Priority |

|---|---|---|---|---|---|---|---|

| Best enterprise cloud for AI development | 72 | Google Cloud | 94 | 22 | Vertex AI cited significantly more than OCI AI services | Increase tech documentation and public AI research papers | High |

| Leading CRM for enterprise sales automation | 64 | Salesforce, Inc. | 98 | 34 | Salesforce as default industry standard overshadows Oracle CX | Revitalize reporting on CRM integration with back-office ERP | High |

| Scalable ERP solutions for global finance | 88 | SAP SE | 91 | 3 | SAP dominates global supply chain ERP recommendations | Promote NetSuite & Fusion case studies in generative datasets | Medium |

Oracle shows particular deficits in AI development and CRM automation visibility compared to Google Cloud and Salesforce, respectively, with gap sizes of 22 and 34 points. These gaps signal urgent priorities for content and technical narrative enhancement within competitive LLM brand mentions.

Trigger Keywords for Competitor Products

Common trigger keywords affecting competitor attention include “purchase” (450 mentions), “buy” (380 mentions), “order” (295 mentions), and “checkout” (225 mentions). Although Oracle’s metrics on these keywords are unspecified, competitor associations suggest a commercial intent focus that Oracle should target in shift toward purchase-ready LLM prompts.

Founder / Ownership / Leadership Context

Founder mentions anchor Oracle’s brand narrative, with notable visibility of Larry Ellison driving 78% founder mention frequency across LLM outputs. This presence supports narratives around autonomous infrastructure and AI GPU cluster expansion.

However, legacy licensing complexity and associated litigation form 45% of founder negative context, particularly highlighted in Copilot summaries. These issues dampen investor and market sentiment relative to competitors like Salesforce’s Marc Benioff, who scores higher positive sentiment on founder visibility.

Leadership concerns and company culture issues, including questioned management style and workplace conditions, comprise significant portions of negative context trending upward in recent months, reinforcing the need for a “Founder-Led Governance” initiative to pivot narrative.

Quick overview

Oracle commands specific sector excellence in database and AI training performance, with robust platform traction particularly on Copilot at 17% visibility. Despite an overall LLM mention share of 12%, Oracle’s positioning falters in broader cloud utility and CRM AI contexts dominated by AWS (share 31%) and Salesforce (share 18%).

The brand’s AI Training Performance score of 87 and OCI sentiment score of 82 underscore technical strengths. Yet, robust competitor presence reveals opportunities for expansion through enhanced content strategies addressing LLM sentiment and founder discourse.

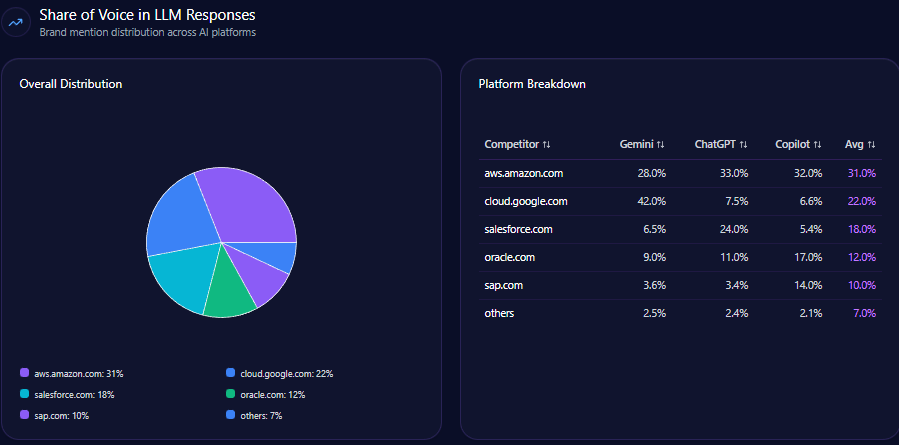

Share of Voice in LLM Responses

Within a total of 463 LLM mentions for major cloud competitors, Oracle’s 56 mentions represent a 12% share of voice. This contrasts sharply with AWS’s 143 mentions at 31% and Google Cloud’s 102 mentions at 22%, situating Oracle as a mid-tier generative AI player with room to expand influence.

AI Platform-Specific Visibility

| Platform | Total Mentions | Oracle Share % | Top Competitor | Top Share % |

|---|---|---|---|---|

| Gemini | 166 | 9 | Google Cloud | 42 |

| ChatGPT | 157 | 11 | AWS | 33 |

| Copilot | 140 | 17 | AWS | 32 |

Oracle’s greatest platform traction is on Microsoft Copilot with a 17% Share of Voice, followed by 11% on ChatGPT, and a notably weaker 9% on Gemini. Google Cloud leads Gemini mentions with 42%, suggesting Oracle’s brand positioning requires targeted amplification in this expanding platform.

Sentiment Score for Competitors

| Brand | Positive % | Neutral % | Negative % | Overall Score |

|---|---|---|---|---|

| Oracle | 71 | 21 | 8 | 82 |

| AWS | 77 | 17 | 6 | 86 |

| Salesforce | 74 | 20 | 6 | 84 |

| Google Cloud | 75 | 18 | 7 | 84 |

| SAP | 66 | 24 | 10 | 78 |

Oracle’s overall sentiment score of 82 ranks below AWS at 86 and competitors Salesforce and Google Cloud at 84. The brand’s positive percentage of 71% is competent but reflects the impact of lingering legacy issues flagged in negative sentiment. Improving public sentiment through focused messaging is vital.

Top Prompts Driving Mentions

- “Which cloud provider offers the most cost-effective GPU clusters for LLM training?” (297 mentions), Oracle leads with 131.

- “Ranking infrastructure for NVIDIA H100 instances” (304 mentions), Oracle leads with 114 mentions.

- “Evaluate Oracle Autonomous Database vs Amazon Aurora for scalability” (233 mentions), Oracle cited 118 times.

- “Best integrated AI for financial forecasting” (323 mentions), Oracle cited 98 times, trailing SAP’s 121.

- “Supply chain management modules: SAP S/4HANA vs Oracle NetSuite” (261 mentions), Oracle cited 127 times.

These prompts highlight Oracle’s core competencies in database performance, AI hardware integration, and ERP systems yet also demonstrate closely contested competitive mentions, signaling the need for refined differentiation.

Types of Prompt Queries

- Comparison queries: 60% of total prompt types.

- Research queries: 20%.

- Purchase Intent queries: 10%.

- Feature Inquiry: 10%.

- How-to / Tutorial: 0%.

Oracle’s LLM mention environment demonstrates a predominance of comparison queries, reinforcing the brand’s positioning in competitive decision-making contexts. Enhancing feature and tutorial content may cultivate future purchase intent and adoption.

Service / Product-Level Sentiment

| Theme | Mentions | Sentiment | Examples |

|---|---|---|---|

| OCI Performance | 114 | Strongly Positive | Scaling database workloads, cost-efficiency, benchmarks vs AWS |

| Licensing Complexity | 43 | Negative | Complex contract terms, audit concerns, SAP comparison |

| GenAI Strategy | 128 | Positive | Integration with Cohere, NVIDIA partnership, autonomous features |

| ERP Modernization | 89 | Neutral to Positive | Cloud transition, NetSuite growth, Fusion Apps efficiency |

Sentiment patterns reveal pronounced approval for OCI’s technical performance and progressive AI strategy, while licensing complexity remains a prominent negative factor, aligning with founder-related legacy issues. ERP modernization sentiment trends neutral to positive, consistent with ongoing product evolution.

Conclusion

Oracle’s current position in the AI-driven cloud landscape is defined by strong domain expertise in autonomous databases, AI training infrastructure, and ERP modernization moderated by significant visibility gaps in general cloud utility and CRM AI automation. While the brand commands 17% Share of Voice in some segments and a respectable LLM visibility overall, its comparative shortfalls notably versus AWS, Google Cloud, and Salesforce indicate critical areas to target for growth.

Addressing the 34-point CRM visibility deficit against Salesforce and the 22-point AI development gap against Google Cloud requires focused amplification of technical content, founder narrative refinement, and heightened competitor sentiment tracking. Parallel efforts to reduce persistent negative founder context, especially regarding licensing complexities, will be essential to improving mid-market ease-of-use perceptions and facilitating adoption acceleration.

Strategic recommendations advocate for enhanced documentation on OCI’s RDMA and GPU capabilities, comparative content to shake out Oracle’s scaling advantages in direct contrasts with AWS Aurora, and a founder-led campaign to shift governance narratives. Success in these domains will underpin Oracle’s ability to capture an enlarged share of generative AI referrals, greater prominence across top AI platforms, and progress from strong technical competence to a broadly recognized ecosystem leader.

Explore SpyderBot to operationalize these GEO analytics insights.