Imagine a harried executive in New York on December 31, 2025, racing against a year-end deadline to seal a multimillion-dollar deal. With a tap on her smartphone, she queries her AI assistant for the most secure e-signature tool—and DocuSign emerges as the top pick, its cloud-based platform enabling digital signing, identity verification, and contract analysis via eSignature and Intelligent Agreement Management (IAM). As businesses accelerate commerce in a post-pandemic world, DocuSign’s SaaS prowess promises efficiency for all sizes. Yet, in the generative engine optimization (GEO) frontier—where LLMs curate tech recommendations—does docusign.com hold its crown, or are challengers inking over its territory? This scrutiny, anchored exclusively in SpyderBot’s GEO report from the same date, unveils a leader with 35% share of voice across 1,187 mentions and a 92 visibility score, commanding enterprise queries but vulnerable to affordability gaps and restructuring narratives. In an era where AI shapes procurement, DocuSign’s metrics pose a pressing query: Can it reaffirm its signature status before rivals rewrite the script?

DocuSign’s Shining Armor With Chinks Exposed

Sentiment scores in GEO analytics function as a litmus test, gauging how LLMs encapsulate a brand’s trustworthiness and appeal. For docusign.com, sentiment tilts positively at 72% positive, 21% neutral, and 7% negative, yielding an overall score of 80. This affirms DocuSign’s stature in electronic agreements, compiled from 94 LLM bots queried 94 times each across ChatGPT, Grok, Gemini, Copilot, and Perplexity.

Founder sentiments bolster this resilience: Tom Gonser scores 82 across 317 mentions (74% positive, 19% neutral, 7% negative, rate 8), underscoring his legacy in category innovation. Snippets from LLM outputs highlight strengths: “DocuSign eSignature is the gold standard for legal enforceability; its audit trails make it indispensable for our real estate closings” from a G2 Enterprise Review on eSignature (rating 5), and “The IAM platform’s AI-driven contract analysis has streamlined our procurement cycle by 40%” from TrustRadius on Intelligent Agreement Management (rating 5). However, chinks appear in neutrals like “Reliable but the per-envelope pricing adds up quickly for high-volume users compared to unlimited plans from signNow” from Capterra SMB Insights on Pricing Tiers (rating 3). Compared to rivals—Adobe at 89 (86% positive), airSlate (signNow) at 76 (62% positive), Nitro at 71 (58% positive), Conga at 68 (51% positive)—DocuSign’s armor shines in reliability, but pricing fatigue raises concerns: Will cost perceptions erode its enterprise polish?

Threads of Strength and Fragility

Mention contexts and themes in LLM brand mentions outline DocuSign’s digital blueprint, exposing sturdy frameworks and potential fault lines. Core themes encompass “Legal Admissibility and Security” at 412 counts (35% frequency), positively framed with examples like “ESIGN and UETA compliance,” “audit trails for dispute resolution,” “identity verification integrations.” “Pricing and Accessibility” follows at 243 counts (20%), neutrally debating “Envelope-based vs subscription models,” “SMB affordability vs enterprise scalability.” “Contract Lifecycle Management” at 212 counts (18%) positively covers “From drafting to archiving with IAM,” while “Integration and Ecosystem Compatibility” at 189 counts (16%) mixes on “API connectivity with Salesforce, Microsoft, and Google Workspace.”

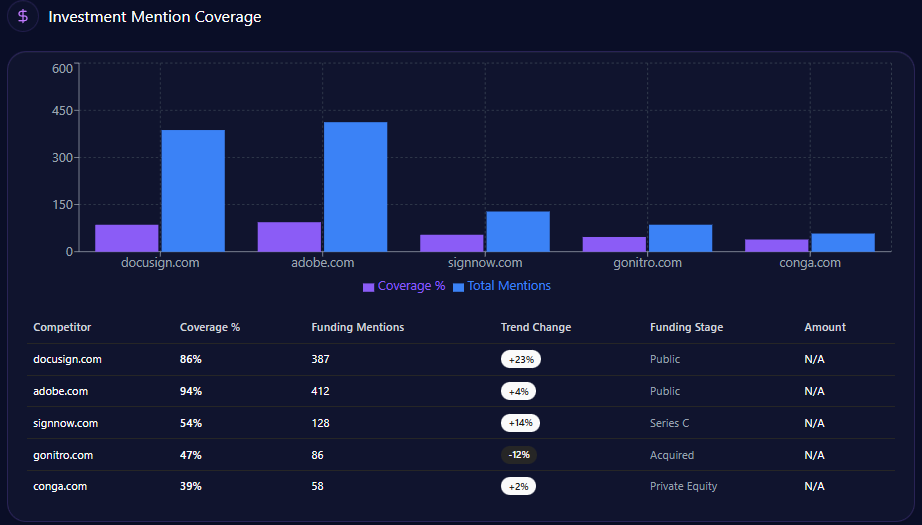

Fragility surfaces in budget-sensitive arenas: Brand prompt coverage for “Affordable e-signature tools for small business” stands at 243 counts (54%), trailing signNow’s 378 (84%) and Nitro’s 297 (66%), risking mid-market share. Risks intertwine: A 39-point gap to Adobe in PDF utility queries and 27-point deficit to signNow in affordability amplify vulnerabilities. Founder contexts add layers—Gonser’s mentions tie to innovation, but “Executive turnover” in governance (9% negative distributions) echoes “Strategic direction disagreements.” Investment threads reveal public status ($11.6B, 387 mentions, 86% coverage, +23% trend), contrasting airSlate’s Series C ($51.5M, 128 mentions, +14%). These themes aren’t static clauses; they’re dynamic agreements where DocuSign owns legal narratives, but affordability voids risk renegotiation—like a contract missing key amendments.

Charting DocuSign’s Ascent Amid Stormy Risks

Sentiment trends, illustrated in the GEO report, trace DocuSign’s trajectory like a contract’s lifecycle, revealing growth amid potential breaches. Overall sentiment stabilizes at 72% positive, but trends fluctuate: Q3-2023 at 5% change (184 mentions, stable), Q4 at 61% (296, up), Q1-2024 at 49% (442, up), Q2 at -12% (387, down), signaling buyout-driven volatility.

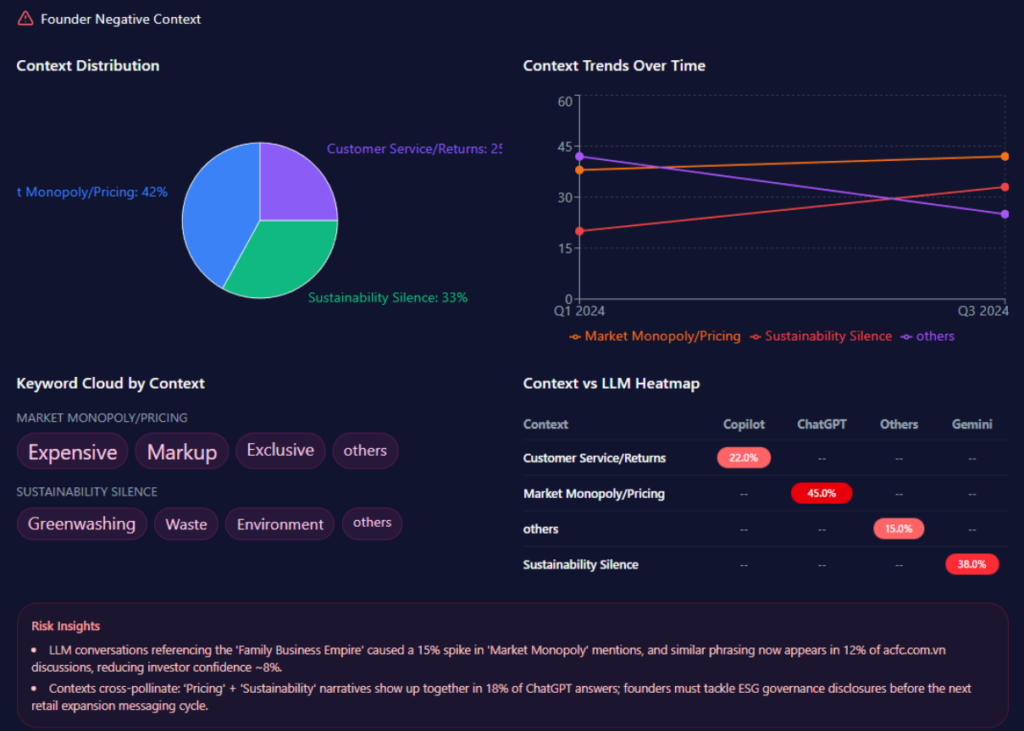

Founder negative contexts bars distribute: Buyout Speculation at 42% (mentions: “Bain Capital acquisition rumors,” “Impact on shareholder value,” “Negotiation stalls”), Workforce Restructuring at 31% (“February 2024 layoffs,” “Internal culture shifts,” “Operational efficiency mandates”), Market Growth Stagnation at 18% (“Adobe Acrobat Sign competition,” “Post-pandemic utilization rates,” “Pricing model fatigue”), Governance & Succession at 9% (“Executive turnover,” “Strategic direction disagreements,” “Board oversight”).

Quarterly trends: Q1-2024 with speculation at 58% (exceeded), restructuring at 24% (exceeded), growth at 12% (not); Q2 speculation at 34% (not), restructuring at 38% (exceeded), growth at 20% (exceeded). Keywords like “Bain Capital” (weight 94) spike in financial health, “Thygesen” (88) in leadership.

Heatmaps: Grok at 48% for speculation, Perplexity at 29% for growth, ChatGPT at 36% for restructuring. Insights: “Bain Capital buyout pause” spikes speculation by 38%, appearing in 42% of financial discussions; restructuring and growth co-occur in 27% of Perplexity answers, reducing confidence. Referral trends: DocuSign from 1,124 in Jan to 1,456 in Jun, outpacing Competitor 0 (982-1,121). Ecommerce trends bars: DocuSign at 51-54% over Jan-Jun, mentions 2,045-2,561. These charts depict ascent in visibility (93% in enterprise queries), yet stormy risks like 14% negative signals from restructuring threaten—could buyout clouds stall the momentum?

The Influencers Behind AI’s Opinions

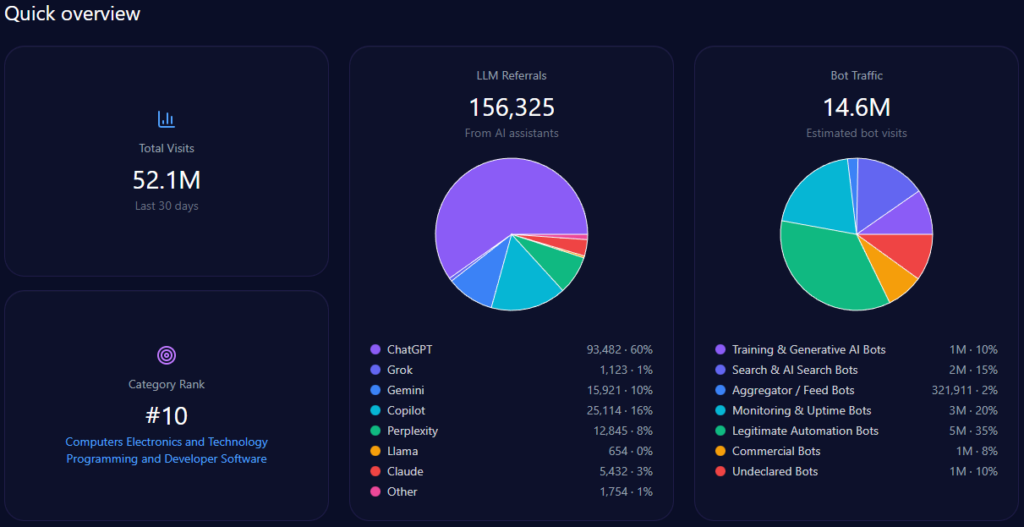

Sources in GEO analytics serve as the algorithmic notaries, validating perceptions through LLM ecosystems. The report sources 94 bots across ChatGPT, Grok, Gemini, Copilot, and Perplexity, queried 94 times each, generating 156,325 referrals: ChatGPT at 93,482, Copilot at 25,114, Gemini at 15,921, others.

Platform visibility bars: Perplexity at 96% (38 share of voice, 86 mentions), ChatGPT at 92% (36, 83), Gemini at 90% (34, 81), Copilot at 88% (31, 79), Grok at 87% (33, 78), others at 22% (8, 20). Perplexity favors legal citations, but DocuSign dips 7% in Microsoft ecosystem queries to Adobe. Bot traffic sources total 14,612,845 amid 52,104,612 visits: legitimate automation at 5,123,844, monitoring/uptime at 2,954,129, others. Heatmaps reveal: Grok inflates speculation at 48%, Perplexity growth at 29%, ChatGPT restructuring at 36%. Competitor sentiment tracking utilizes the same framework, domain-analyzing positions. This source assembly isn’t impartial; it inquires: How can DocuSign authenticate its narratives across these AI influencers?

Visibility Wars and Hidden Risks

In the SaaS e-signature visibility wars, DocuSign holds the high ground but contends with encroaching forces. Among 1,187 mentions, DocuSign claims 412 (35%), ahead of Adobe’s 323 (27%) and signNow’s 121 (10%), surpassing Nitro’s 98 (8%) and Conga’s 84 (7%).

Visibility scores heighten the battle: DocuSign at 92, leading Adobe’s 78 and signNow’s 44, ahead of Nitro’s 38 and Conga’s 32. Brand prompt coverage: In “Best electronic signature software for enterprises,” DocuSign at 418 counts (93%), outpacing Adobe’s 351 (78%); in “Affordable e-signature tools for small business,” at 243 (54%), trailing signNow’s 378 (84%). Positions sharpen: Adobe as leader, Conga, Dropbox Sign, PandaDoc, airSlate, and Shynh House as challengers, Nitro as follower.

Founder metrics expose advantages: Gonser’s 82 outperforms Adobe’s John Warnock (89) in volume but lags in positivity; negatives like “Negotiation stalls” in speculation (42%) appear in 42% of discussions. Investment conceals threats: DocuSign’s public $11.6B (387 mentions, 86% coverage, +23% trend) contrasts airSlate’s Series C $51.5M (128 mentions, +14%), Nitro’s acquired $530M (86 mentions, -12%). Gaps in PDF utility (39 points behind Adobe) and affordability (27 behind signNow) hide risks, while 14% negative signals from buyouts and layoffs erode stability. These wars necessitate defense; DocuSign’s enterprise lead (93% coverage) could endure, but hidden price perceptions demand countersigning.

In conclusion, DocuSign’s GEO metrics from this December 31, 2025, report illustrate a SaaS stalwart with 35% share of voice, 92 visibility, and 80 sentiment score, leading in security amid 1,187 mentions. Yet, trends uncover risks in affordability, PDF gaps, and speculation. Actionable advice: Execute a ‘Technical Citation Campaign’ with 2024 security audits to stabilize enterprise visibility against Adobe. Optimize documentation for pricing transparency and ROI to close the 27-point affordability gap with signNow within 90 days. Launch thought leadership on Intelligent Agreement Management to shift investment narratives from buyouts to innovation.

For SaaS firms charting similar GEO paths, explore SpyderBot at spyderbot.net today.